Chapter 4 - Valuation of Vacant Land Present Worth

Concept of Present Worth Valuation

Assessors are required to consider, and when applicable, to apply the present worth valuation procedure when using the market approach to value vacant land, § 39-1-103(14)(b), C.R.S.

Present worth valuation of vacant land involves discounting. Discounting is defined in The Dictionary of Real Estate Appraisal, 7th Edition, 2022, published by the Appraisal Institute, as a procedure used to convert periodic income, cash flows and reversions into present value. Present value is based on the assumption that benefits received in the future are worth less than the same benefits received now. The objective is to determine the present worth, i.e., the actual (market) value, as of the appraisal date, of the vacant land; not its future value.

Discounting of vacant land establishes the present worth of vacant land that will not likely sell within one year. The reason for vacant land present worth valuation is to account for the time, in years, necessary to sell an inventory of vacant lots, sites, parcels, or tracts. According to Colorado law, the present worth valuation of vacant land is synonymous with actual or market value.

Refer to Definition of Terms at the end of this chapter for explanations of terms used.

It is important to note: throughout this chapter the terms “subdivider” or “land developer” are used to describe owners of vacant land. The terms are not meant to limit the application of present worth valuation procedures to specific types of land ownership. Vacant land owned by private individuals, who are neither subdividers nor developers, are considered for present worth valuation if the land otherwise qualifies.

The Colorado Supreme Court ruled that the Division’s present worth valuation procedure is an appropriate interpretation of the statutes controlling the valuation of vacant land, El Paso County Board of Equalization v. Craddock, 850 P.2d 702 (Colo. 1993). The concept of raw land value being a market value threshold below which present worth values may not decline was referenced in footnote 4, p. 707, of the case.

The Division developed a seven-step present worth valuation procedure. The objectives of the procedure are to:

- Determine the applicability of present worth valuation to the vacant land being valued

- Determine appropriate adjusted selling prices, and

- Determine the present worth value of vacant land

Present Worth Valuation Procedure

All vacant land, whether part of an approved subdivision plat, part of a Planned Unit Development (PUD), part of an environment of competing unplatted properties, or even a single, competitively isolated tract is eligible for present worth valuation. In the following procedures, the terms “lot or tract” or “lots or tracts” refer to all such land.

Applicability Present Worth Valuation

Before vacant land unadjusted selling prices (UASP) are determined, a decision is made as to whether the vacant land present worth valuation procedure applies to the subject property or properties under appraisal. The determination is made in step 2 of the present worth valuation procedure.

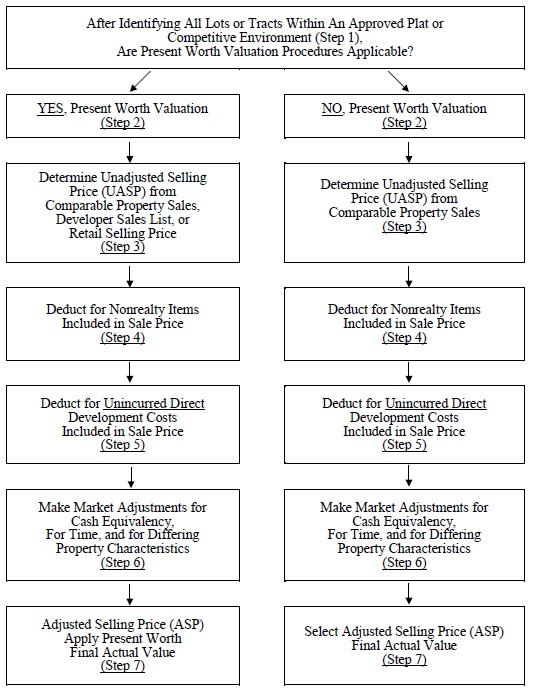

Step #1 Identify all lots or tracts within an approved plat or competitive environment.

Step #2 Determine the applicability of vacant land present worth valuation procedure.

Step #3 Determine the unadjusted selling price (UASP).

All steps in the present worth valuation procedure are illustrated in the following Decision Tree Analysis.

Decision Tree Analysis

Step #1 – Identify all Lots or Tracts Within An Approved Plat

“Vacant land” means any lot, parcel, site, or tract, upon which no buildings or fixtures, other than minor structures, are located, § 39-1-103(14)(c)(I), C.R.S. “Minor structures” means improvements that do not add value to the land on which they are located and that are not suitable to be used for and are not actually used for any commercial, residential, or agricultural purpose, § 39-1-103(14)(c)(II)(A), C.R.S. Vacant land may also include land that contains a non-minor structure as defined in ARL Volume 2, Administrative and Assessment Procedures, Chapter 6, Property Classification Guidelines and Assessment Percentages.

Identifying all lots or tracts within an approved plat or competitive environment is the initial step in determining the applicability of present worth valuation procedures for vacant land.

For the purpose of the procedures, approved plats are defined as:

- For subdivided land, the approved subdivision and/or its approved filings and/or its approved development tracts

- For Planned Unit Developments, the approved plan

Historically, Planned Unit Developments (PUDs), sometimes known as Planned Developments (PDs), are approved plats for the purpose of determining the applicability of present worth valuation. Sometimes these terms are used in a general way to describe zoning. If these terms are used to describe zoning, they are not an approved plat for the present worth valuation procedure.

An approved plat for subdivided land may include one or all filings within the subdivision. A single approved plat may include multiple uses. Commercial and industrial lots or tracts may exist along with residential lots or tracts within the boundaries of the approved plans for Planned Unit Developments.

If separate portions, phases or filings of a subdivision are approved at different times, then each becomes a separate approved plat and absorption calculations for each approved plat are required. To meet the definition of an approved plat, a plat must complete the entire typical approval process of the appropriate governmental entity.

For example, a plat was approved in its entirety on February 1st. The plat includes 115 single family residential lots, 76 townhome lots, and 3 large commercial lots. This one approved plat contains 194 buildable sites. Absorption calculations should be based on an original count of 194 lots. It would be contrary to Colorado law to use separate absorption calculations for the residential, townhome, and commercial lots.

For unplatted land, discounting is based on the environment of a group of competing properties, e.g., multiple contiguous tracts of land of 35 acres or more in size that do not need subdivision approval. Unplatted land can be any tract of land with an established boundary and legal description, and is typically described by section or tracts.

Step #2 – Applicability of Vacant Land Present Worth Procedure

Under § 39-1-103(14)(c)(I), C.R.S., all vacant land is eligible for present worth discounting. As part of the sales verification process, a determination is made as to whether the present worth valuation procedures are applicable to the subject property or properties.

The criteria for determining if present worth valuation is applicable are:

- The procedures are only applied to vacant land.

- Less than 80 percent of the buildable lots, tracts, sites, or parcels within an approved plat or competitive environment have been sold.

- In situations where mixed use has been approved and lot lines are established within a single approved plat, each lot is counted toward the 80 percent sellout threshold regardless of size or use.

- Lots or tracts that have legal or physical no-build restrictions should not be included in the original number of lots or tracts when determining the 80 percent sellout thresholds. These lots or tracts are typically never part of the developer’s “marketable” inventory, and will never be sold. Such lots or tracts, while never available to the open market or subject to present worth valuation, are valued with consideration given to their no-build restrictions. Lots or tracts which might have legal and/or physical no-build restrictions include the following:

- Open space lots or tracts that are required in a subdivision plan before building permits are issued

- Greenbelt lots or tracts that are permanently incorporated within a subdivision plan

- Lots or tracts unbuildable due to city or county building or zoning requirements

- "Out lots” that are adjacent to buildable lots; but due to their size or access problems, are effectively unbuildable

Only sales or long-term leases of lots to “end users” reduce the vacant land inventory and therefore, count toward the 80 percent sellout threshold. “End users” are those parties who intend to, are expected to, or have done one of the following:

- Construct improvements on the vacant lots for themselves or have begun construction of improvements, such as speculative homes, for others

- Purchase improvements constructed by builders for them

- Use the vacant land in conjunction with other improved property under the same ownership

- Purchase the vacant land for investment and intend to withhold the land from the open-market for an extended period of time

NOTE: Since sales to “end users” reduce the vacant land inventory, these sales are used for all absorption calculations, including the 80 percent sellout threshold, absorption rate, and absorption period.

- Bulk lot sales to another subdivider or land developer do not count toward the 80 percent sellout threshold. When a land developer legally transfers ownership of vacant lots in an approved subdivision plat to another land developer, there is no change in the percentage of lots or tracts sold, unless the land is resubdivided or replatted and the number of lots within the original subdivision changes.

- If a replat or resubdivision occurs and the intent of the original subdivision is substantially altered, as with a change in density or zoning, then two approved plats would exist and the total lot counts, absorption rates and periods, and the 80 percent sellout thresholds are recalculated.

- Replats or resubdivisions, which do not substantially alter the intent of the original subdivision, such as a lot line vacation, only require a recalculation of the total number of lots within the original approved plat.

- The absorption period for an approved plat or competitive environment is calculated to be more than twelve months. Absorption periods of more than twelve months are rounded up to the next whole number, so a minimum absorption period of two years is required at each change in level of value. The absorption period represents:

- the years remaining until the approved plat or competitive environment is 100% sold-out or

- the required number of years for a single, competitively isolated tract to sell to an end user.

- The application of present worth valuation procedures produces a value greater than current raw land value as defined in these procedures.

Step #3 – Determine Unadjusted Selling Prices (UASP)

Determining unadjusted selling prices (UASP) is essential to begin the sales adjustment process.

For vacant land the UASP is developed from analysis of data from the following sources:

- The retail selling price listing provided by the developer, subdivider, or property owner at the end of the data collection period.

The selling price is requested in the Vacant/Subdivision Land Questionnaire mailed each year to developers. - Confirmed arm’s-length sales of similar lots or tracts within the subdivision or its filings during the data collection period.

- Sales of other similar lots or tracts by other developers or subdividers within competitive environments or approved subdivisions inside or outside the county during the data collection period. [For direction on using sales outside the county see Board of Assessment Appeals, et al., v. E.E. Sonnenberg & Sons, Inc., 797 P.2d 27 (Colo.1990)]

The UASP is generally the price shown on the Real Property Transfer Declaration (TD-1000) or, if no TD-1000 is filed, on a supplementary confirmation questionnaire. If no supplementary questionnaire is returned, then the documentary fee sales price is used, assuming that the sale is otherwise qualified. However, the UASP should not fall below the most comparable current raw land value.

Future projections of sales prices need not be made by assessors due to the following reasons:

- For the purpose of the procedure, site values during the current data-gathering period are assumed to remain stable over time.

- Since assessing officers in Colorado are required to review vacant land present worth procedures for each change in level of value, modifications to selling prices are made every other year.

The only change required in intervening years, other than for an unusual condition, is to reduce the absorption period by one year. Then, recalculate the present worth actual value for the intervening year using the present worth factor for the modified absorption period. The sellout percentage and absorption rate calculations remain unchanged, unless a substantial resubdivision has occurred. For absorption periods calculated to be two years at a change in level of value, the absorption period will be one year in an intervening year.

EXCEPTION: If the number of sales within the approved plat, for the 12 months following the current appraisal date, is less than the absorption rate per year calculated for the plat, the absorption period may be left unchanged.

- Projection of future market activity is highly speculative.

Determining Appropriate Adjusted Selling Prices

Reviewing steps 4 through 6 (as shown on the decision tree), they are identical whether or not present worth valuation is applicable.

Step #4 Deduct for nonrealty value included in the sale price.

Step #5 Deduct unincurred direct development costs included in the sale price. The costs are for items not installed as of the assessment date, but included in the sales price.

Step #6 Make market adjustments to determine the adjusted selling price (ASP).

Step #4 - Deduct for Nonrealty Value Included in the Sale Price

By removing all nonrealty items, deductions are made to comparable properties’ unadjusted selling prices (UASP) to achieve the correct real property market value, or actual value of the real property.

Isolation of realty is accomplished prior to making any financing or property characteristic adjustments for differences between the comparable property sales and the subject property.

Example:

Deduction of the market value for nonrealty items to determine the price paid for the real property portion of the sales price

| Total Sales Price (documentary fee and TD-1000) | $40,000 |

|---|---|

| Deduction - Less Nonrealty Item (Fishing Club Membership included in purchase price) | - 7,500 |

| Total Adjusted Sales Price | $32,500 |

Step #5 - Deduct Unincurred Direct Development Costs in the Sale Price

Deductions are then made for any unincurred direct development costs. These are the costs of site improvements and direct construction costs that were included in the sales price, but were not installed as of the assessment date.

Statute requires that adjustments be made for unincurred direct costs of development before making market adjustments to vacant land sales for cash equivalency, for time, and for differing property characteristics.

Actual value determined - when.

(14)(b) The assessing officers shall give appropriate consideration to the cost approach, market approach, and income approach to appraisal as required by the provisions of section 3 of article X of the state constitution in determining the actual value of vacant land. When using the market approach to appraisal in determining the actual value of vacant land as of the assessment date, assessing officers shall take into account, but need not limit their consideration to, the following factors: The anticipated market absorption rate, the size and location of such land, the direct costs of development, any amenities, any site improvements, access, and use. When using anticipated market absorption rates, the assessing officers shall use appropriate discount factors in determining the present worth of vacant land until eighty percent of the lots within an approved plat have been sold and shall include all vacant land in the approved plat. For purposes of such discounting, direct costs of development shall be taken into account. The use of present worth shall reflect the anticipated market absorption rate for the lots within such plat, but such time period shall not generally exceed thirty years. For purposes of this paragraph (b), no indirect costs of development, including, but not limited to, costs relating to marketing, overhead, or profit, shall be considered or taken into account (emphasis added) .

§ 39-1-103, C.R.S.

Lump sum dollar adjustments, rather than percentage adjustments, should be used. However, lump sum dollar adjustments should be carefully documented and compared to the adjusted selling price (ASP) of comparable completed lots or tracts to avoid errors in valuation.

For present worth procedures, the vacant land value reflected in the ASP must not fall below the most comparable value of raw land.

Development costs are divided into two categories:

- Direct development costs

- Indirect development costs

Direct Development Costs:

- Curbs and Gutters Streets

- Culverts

- Sanitary and Drainage Sewer Facilities

- Street Lighting

- Utility Easements & Hookup

- Utilities Installation

- Site Preparation and Grading

- Sidewalks

- Environmental Compliance Costs

- Soil Tests

- Engineering and Surveying Costs

- Permits, Fees (Including Tap Fees) and Performance Bond Costs

- Insurance Directly Related to Development Construction

- Greenbelt and Common Area Development including Landscaping

Indirect Development Costs*:

- Sales Marketing Costs

- Sales Commission Costs

- Guest Generation Costs

- Entrepreneurial Profit

- Owners Insurance Costs

- Project Financing Costs

- Developer/Subdivider Profit

- Holding Costs

- Sales and General

- Administrative Overhead

- Taxes

- Professional Services

- Warranties

* Deductions not allowed pursuant to § 39-1-103(14)(b), C.R.S.

Step #6 - Market Adjustments to Determine Adjusted Selling Price

Since comparable sales are seldom exactly like the subject property, there will be differences to adjust for when making market comparisons. The market adjustments result in the adjusted selling price (ASP).

Market adjustments made for nonrealty items included in the sale are accounted for in Step # 4. The remaining considerations: (1) cash equivalency, (2) market conditions (time), (3) location, and (4) physical characteristics, are summarized into three categories:

- Cash Equivalency: Adjustments are required for atypical financing or sales concessions

- Time: Adjustments for time, i.e., adjusting sales to the appraisal date

- Property Characteristics: Adjustments for property characteristics, e.g., location, access, topography, soil conditions

Market adjustment is the process of adjusting differences in the comparable sales so that they become as similar as possible to the subject property. Adjustments are applied to the sales prices of the comparable properties. The adjusted sales prices then become indicators of value for the subject property.

If the number of valid sales is limited, it is better to adjust sales than to delete sales from the analysis.

Note: It is usually better to gather sales from the full 60-month allowable data collection period and time adjust them to the end of the current data collection period, before using sales that will require a location adjustment.

Refer to Chapter 2, Appraisal Process, Economic Areas, and the Approaches to Value for a complete discussion of how comparable properties are identified and how these adjustments are made.

Adjustments to sales prices should be carefully analyzed and documented before use. The vacant land value reflected in the ASP must not fall below the actual value of the most comparable raw land.

Step #7 - Apply Present Worth Procedures

Determining Present Worth of Vacant Land

The market absorption (sellout) period and discount rate are determined. Both are described under Sales Comparison Method found later in this chapter.

All pertinent information, approved plat or competitive environment, the unadjusted selling price, adjusted selling price, and present worth calculations shall be documented, § 39-1-103(5)(a), C.R.S.

Raw Land Value

Vacant land present worth actual value must never drop below the actual value of the most comparable raw, undeveloped vacant land as of the appropriate level of value.

According to The Dictionary of Real Estate Appraisal, 7th Edition, 2022, raw land is, “land that is undeveloped; land in its natural state before grading, draining, subdivision, or the installation of utilities.”

The Division policy of “raw land value establishing market value when present worth valuation procedures result in a lower value” is the control to ensure that mistakes in application of present worth procedures do not result in the actual value falling below market value as of the appraisal date. Should "discounted vacant land value” drop below market value, inequity in the valuation of vacant land would exist.

The policy is applicable to each level in the valuation process: the unadjusted sale price (UASP), the adjusted sale price after-market adjustments (ASP), and actual value after applying present worth valuation procedures.

Raw land is typically appraised on a per-acre basis although it may be apportioned to lots or tracts on a square foot or site basis when determining whether or not present worth values exceed raw land values. If the original tract has been subdivided, each of the subdivided lots receives an appropriate share of the raw land value for comparison purposes.

Raw land value is the indicated market value of the unimproved vacant land tract adjusted to the current level of value. When determining the raw land value threshold, consideration is given to the three approaches to value; however, since cost and income data are frequently unavailable, reliance is usually placed on the sales comparison method. When determining raw land value, comparable sales should be selected for similarity to the subject tract.

The value of raw land may vary depending upon entitlements. According to The Dictionary of Real Estate Appraisal, 7th Edition, 2022, entitlements are, “In the context of ownership, use, or development of real estate, governmental approval for annexation, zoning, utility extensions, number of lots, total floor area, construction permits, and occupancy or use permits.”

Typically, as more entitlements are obtained for land, its value increases. This explains why farm land in a particular economic area may sell for $3,500 per acre, and a similar contiguous tract of farm land may sell for $20,000 per acre. In this economic area, the market value of raw land may range from $3,500 to $20,000 per acre depending on the level of entitlements. Land that is determined to be raw can still have a wide range of values depending on the extent of entitlements associated with that land. It is important for the assessor to be aware of the entitlements associated with the property being appraised and to establish the raw land “value floor” for that property based on comparison with raw land sales with a similar level of entitlements. It is the assessor’s responsibility to determine which market value is the correct value floor to ensure that the present worth value does not fall below this level.

Vacant/Subdivision Land Questionnaire

For each subdivision, filing, or other approved plat, and for tracts within a competitive environment, data is collected and reviewed annually by the assessor. The data is used to establish absorption periods and adjusted selling prices.

The proper valuation of vacant land under development is very difficult to determine when there is a lack of necessary information. To aid in the solution of this problem, Addendum 4- A, Vacant/Subdivision Land Questionnaire, was developed to collect necessary information from all land developers in the county, including information regarding the valuation of unplatted vacant land.

The assessor mails or delivers, as soon after January 1 as possible, two copies of the Vacant/Subdivision Land Questionnaire to each land developer known or believed to own vacant land in the county. The developer has until March 20 to file the completed questionnaire with the assessor.

Actual value determined - when.

(14)(d) As soon after the assessment date as may be practicable, the assessor shall mail or deliver two copies of a subdivision land valuation questionnaire for each approved plat within the county to the last-known address of the subdivision developer known or believed to own vacant land within such approved plat. Such questionnaire shall be designed to elicit information vital to determining the present worth of vacant land within such approved plat. Such subdivision developer or his agent shall answer all questions to the best of his ability, attaching such exhibits or statements thereto as may be necessary, and shall sign and return the original copy thereof to the assessor no later than the March 20 subsequent to the assessment date. All information provided by the subdivision developer in such questionnaire shall be kept confidential by the assessor; except that the assessor shall make such information available to the person conducting any valuation for assessment study pursuant to section 39- 1-104 (16) and his employees and the property tax administrator and his

employees.§ 39-1-103, C.R.S.

For statewide consistency, the Division recommends each county use the questionnaire. The assessor may request additional information from the taxpayer at any time during the year, § 39-5-115(1), C.R.S. Should additional information be requested either in the cover letter or as a supplemental questionnaire, we recommend that the assessor include the Division’s questionnaire for the land developer’s signature.

The information acquired is updated each year in six-month increments so that all vacant land sales are accounted for throughout the entire length of a possible 60-month data collection period. This is the reason for sending questionnaires during an intervening year. The data returned cannot be used until the following change in level of value.

If any land developer does not return the questionnaire by March 20, the assessor may determine a valuation using the best information available. Should the necessary information be made available during review and appeal, the assessor must consider it.

Actual value determined - when.

(14)(e) If any subdivision developer fails to complete and file one or more questionnaires by March 20, then the assessor may determine the actual value of the taxable vacant land within an approved plat which is owned by such subdivision developer on the basis of the best information available to and obtainable by the assessor.

§ 39-1-103, C.R.S.

Present Worth Valuation Methods

Of the five generally accepted land valuation methods in use by appraisers, described in Chapter 2, Appraisal Process, Economic Areas, and the Approaches to Value, vacant land present worth valuation procedures involves only two. The two are the sales comparison method and the anticipated use or developmental cost method.

Sales Comparison Method

Whenever adequate quantities of qualified sales data are available, direct sales comparison is the best method to value vacant land.

When 80 percent of the lots or tracts are sold, typically, a definitive market value per lot or tract is established. The appropriate unit of comparison value, as adjusted for differing property characteristics, is extended to all vacant lots or tracts in an approved plat or competitive environment. The qualified sales are used as the primary basis for valuing all the lots or tracts regardless of ownership.

The appropriate level of value is used with consideration given to, and adjustments made for, each individual lot or tract's location, desirability, and use. The only change required in intervening years, other than for an unusual condition, is to reduce the absorption period by one year. Then, recalculate the present worth actual value for the intervening year using the present worth factor for the modified absorption period. The sellout percentage and absorption rate calculations remain unchanged, unless a substantial resubdivision has occurred. For absorption periods calculated to be two years at a change in level of value, the absorption period could be one year in an intervening year.

EXCEPTION: If the number of sales within the approved plat, beginning the July 1 following the appraisal date, for 12 months, is less than the absorption rate calculated for the plat, the absorption period may be left unchanged.

If nonrealty items or unincurred direct development costs are included in the sales price of the lot or tract, appropriate deductions must be made to the sales price before making market adjustments.

Refer to Step #5 - Deduct Unincurred Direct Development Costs Included in the Selling Price, earlier in this chapter, for a discussion of appropriate deductions for unincurred direct development costs.

The following process is used when applying the market approach:

- Identify all lots or tracts within an approved plat or competitive environment.

- Determine the actual value of raw land before development.

- Determine the adjusted selling price.

- Determine the absorption period.

- Determine a discount rate and apply present worth procedures to the adjusted selling price.

Identify All Lots or Tracts Within An Approved Plat

All vacant land is eligible for present worth valuation.

Identifying the lots or tracts within an approved plat or competitive environment includes collection, confirmation, and analysis of sales from county records and from the data collected on the Vacant/Subdivision Land Questionnaire.

The guidelines for the county sales confirmation program are found in Chapter 3, Sales Confirmation and Stratification.

The guidelines are used in the confirmation of vacant land transactions. All sales of vacant land whether platted, in development tracts, or unplatted are listed.

Unplatted tracts of land may be competing with more widely scattered parcels. Because of this, competitive environments are determined on a case-by-case basis. Establishing these competitive environments serves two purposes:

- Establishing the overall percentage of market absorption of tracts and

- Establishing the market absorption rates associated with the competitive environment.

Competitive environments are established for unplatted tracts only. A parcel or parcels of land should not be included in both an approved plat and a competitive environment.

To identify the boundaries of the competitive environment, the surroundings of the subject property are examined. Establishing measurable boundaries allows the appraiser to identify comparable properties in the same competitive environment, to track sales activity, and to measure the level of historical absorption of available properties, i.e., vacant land lot or tract sales in the marketplace.

Competition defines competitive environments. Where tracts can reasonably be expected to compete with one another, they are in the same competitive environment, even if the tracts are noncontiguous. Competing tracts generally can be identified through discussions with real estate professionals, recent purchasers of similar tracts, land developers, and property appraisers in surrounding counties.

Competitive environment research begins with the subject property and proceeds outward, identifying all relevant factors and influences on the property's value. The search is generally extended far enough to include all influences that the market perceives as affecting value, i.e., what potential sellers and buyers desire.

The application of present worth to competitively isolated tracts of land may be handled differently, as described later in this chapter.

Determine the Actual Value of Raw Land Before Development

The actual value of the raw land within an approved plat or competitive environment is determined by consideration being given to the most comparable raw land sales adjusted to the current level of value.

The present worth value must never drop below the most comparable actual value of raw, undeveloped vacant land at the current level of value. Raw undeveloped vacant land value is the value of the tract before subdividing, adjusted to the current level of value.

To determine the appropriate raw land value, comparability of sales is essential. The assessor attempts to find sales of similar size and development status.

When analyzing sales for size adjustment, the comparable sold properties must have the same development potential as the subject. Large variances in size typically indicate a different development potential and that the properties are not directly competitive.

Comparable tracts are placed in size ranges, e.g., 1 to 3 acres, 5 to 10 acres, 20 to 35 acres. Since comparable sales are seldom exactly like the subject property, there will be differences to adjust for when making the comparison. Property characteristics are determined and collected for all parcels, both sold and unsold, within an approved plat or competitive environment.

Determine the Adjusted Selling Price

The adjusted selling prices of lots or tracts are determined as follows:

- Collect and confirm comparable sales. Adjustments for nonrealty items are made to isolate the real property and to determine unadjusted selling prices (UASP).

If comparable sales are not available, the assessor considers comparable sales in other approved plats or competitive environments, economic areas, or across county lines. These sales may need adjustment for locational differences.

Refer to Chapter 3, Sales Confirmation and Stratification.

- Select appropriate units of comparison.

- Determine market adjustments to the sales data to reflect the physical characteristics of the subject properties. The process results in the adjusted selling prices (ASP) of subject properties. Refer to Chapter 2, Appraisal Process, Economic Areas, and the Approaches to Value.

The categories of market adjustments considered for vacant land are as follows:

- Cash Equivalency

- Time

- Property characteristics

- Location

- Amenities

- Size

- Access

- Topography

- Other physical characteristics

Other adjustments include, but are not limited to, zoning, engineering, and infrastructure.

All adjustments are applied to sold lots or tracts within an approved plat or competitive environment. The adjusted selling prices of the sold properties serve as base lot or tract values and are applied to the unsold properties. All adjustment amounts or percentages are related to the current level of value.

Determine the Absorption Period

For every reappraisal, the assessor determines the remaining absorption (sell-out) period for the vacant lots or tracts. The calculation is made as of the June 30 appraisal date preceding the change in level of value.

The only change required in intervening years, other than for an unusual condition, is the reduction of the absorption period by one year. Then, recalculate the present worth actual value for the intervening year using the present worth factor for the modified absorption period. The sellout percentage and absorption rate calculations remain unchanged, unless a substantial resubdivision has occurred. For absorption periods calculated to be two years at a change in level of value, the absorption period is one year in an intervening year.

EXCEPTION: If the number of sales within the approved plat, beginning July 1 following the appraisal date, for 12 months, is less than the absorption rate calculated for the plat, the absorption period may be left unchanged.

- Sellout Percentage (Threshold)

To determine whether the vacant land present worth procedures are applied, the sellout percentage is calculated. The calculation is performed by dividing the total number of lots or tracts sold or leased (numerator) by the total number of lots or tracts that are available for sale (denominator). This calculation is made as of the current appraisal date. It is not proper to recalculate this percentage in an intervening year, unless a substantial resubdivision has occurred.

If 80 percent or more of the lots or tracts are sold, all land within an approved plat or competitive environment is valued with consideration given to the three approaches to value and present worth valuation is not applied.

If the sellout percentage is less than 80 percent and the other three criteria are met; (1) the land is vacant, (2) the absorption period is greater than one year, (3) the value is greater than raw land value; then vacant land present worth valuation procedures are applied.

- Absorption Rate

In order to determine an absorption period, it is necessary to first determine the absorption rate. The absorption rate is the rate at which properties are sold within a given area. The rate is usually calculated in sales per month and then annualized by multiplying the result by twelve. The period of time used for calculation of the absorption rate is based on the data collection period from the beginning date of the collection period to the appraisal date. If there is insufficient sales history, the absorption rate of a comparable approved plat is used.

The beginning date for marketing of lots or tracts is sometimes used for new developments. If lots in an approved plat begin selling after the beginning of the 18- month data collection period, but before the end of the data collection period, the same number of months that the lots or tracts are available for sale is used to calculate the absorption rate.

For subdivisions without sales data or for those formed after the June 30 appraisal date, absorption rates from comparable subdivisions are used. Sales that may have occurred after the appraisal date may be used as a check to ensure that the comparable subdivision’s absorption rate is truly comparable.

If no comparable subdivisions exist, it is assumed that at least one sale has occurred during the data collection period.

Example:

For an 18-month sales data collection period

1 (sale) ÷ 18 (months) = .0555 the monthly absorption rate

.0555 X 12 (months) = .6666 the absorption rate (annualized).

The annual absorption rate divided into the number of lots or tracts remaining to be sold on the June 30 appraisal date, when rounded to the next whole number, results in the absorption period used for the approved plat.

This calculation is made as of the current appraisal date. It is not proper to recalculate this percentage in an intervening year, unless a substantial resubdivision has occurred.

- Absorption (Sellout) Period

The absorption (sellout) period is the number of years during which vacant lots or tracts are expected to be sold within an approved plat or competitive environment, or the number of years required to sell a single, competitively isolated tract of land as a unit.

This time period is calculated by dividing the number of remaining lots or tracts to be sold by the absorption rate and then rounding up to the next whole number. In the case of a tract of land being sold as a unit, the estimated number of years to the sales date is rounded up to the next whole year. The period is expressed as the whole number of years necessary to sell the remaining vacant lots or tracts. Absorption rates from comparable subdivisions should be used to calculate the absorption period for approved plats formed after the June 30 appraisal date.

Since one of the present worth criteria requires an absorption period of greater than 12 months from the appraisal date, the minimum absorption period is two years as of the appraisal date. The minimum absorption period in an intervening year is one year.

Absorption Calculations

Both the absorption rate and absorption period are calculated by following the process

described below.

- Identify all lots or tracts within an approved plat or competitive environment.

- Approved plats and competitive environments are analyzed each reappraisal cycle. The analysis takes into consideration the sales pattern experienced within the area during the sales data collection period.

- Narrative descriptions and supporting documentation should accompany all approved plat and competitive environment analysis and subsequent changes.

- Transamerican Realty Corporation v. Clifton, 817 P.2d 1049 (Colo. App. 1991) requires that the assessor provide adequate documentation as evidence to support the values established for all applicable approaches to appraisal. Insufficient time is not a reasonable excuse for failure to consider the applicable approaches to value.

- If additional information is needed, refer to Step #1 - Identify All Lots or Tracts Within An Approved Plat or Competitive Environment earlier in this chapter.

- Determine the total number of lots or tracts within an approved plat or competitive environment.

- The total numbers of sold and unsold lots or tracts within an approved plat or competitive environment are used in calculating the sold percentage, the absorption rate and the absorption period. Consult local real estate professionals to determine the length of time necessary to sell a single, competitively isolated tract.

- Determine the total number of lots or tracts conveyed.

- The number of vacant lots or tracts sold and vacant lots or tracts under longterm leases are totaled. Lots under long-term lease include those that may have been leased to persons intending to install manufactured housing on permanent foundations or to build other improvements.

- Lots or tracts under installment land contracts are considered sold solely for the purpose of determining absorption calculations. The assessor contacts each developer to determine if any lots or tracts have installment land contracts and to obtain a list of the contract sales.

- For a statutory appraisal year and for the following intervening year, the data collection period can be a total of sixty months, i.e., the 60-month data collection period allowed in sales comparison analysis, § 39-1-104(10.2)(d), C.R.S.

- Calculate the sellout percentage, the absorption rate, and the absorption period.

- It is important to calculate the sellout percentage first. If the sellout percentage is 80% or greater, present worth procedures do not apply. It is necessary to calculate the absorption rate in order to determine the absorption period.

The absorption rate calculation is based on the number of lots or tracts sold during the preceding data collection period. The period used to calculate the absorption rate is the same as that used for collecting sales data. For approved plats without sales data, or for those formed after the June 30 appraisal date, absorption rates from comparable approved plats with sales during the data collection period are used to establish the absorption rate. - The sellout percentage calculation:

- Divide the number of lots or tracts sold within an approved plat or competitive environment by the total number of saleable lots or tracts within the approved plat or competitive environment. This number must fall below the 80% sellout threshold to qualify for the discount

For older developments, the recommended number of months is the minimum sales data collection period of 18 months. The maximum number of months is 60.

- Divide the number of lots or tracts sold within an approved plat or competitive environment by the total number of saleable lots or tracts within the approved plat or competitive environment. This number must fall below the 80% sellout threshold to qualify for the discount

- The absorption rate calculation:

- Divide the number of sales within the data collection period by the number of months within the data collection period. This is the average absorption rate per month.

- Multiply the average absorption rate per month by 12 to determine the annual absorption rate.

If no sales within an approved plat or competitive environment exist, and there are no similar approved plats or competitive environments, it is assumed that at least one sale occurred during the data collection period so that an absorption rate can be calculated.

- The absorption period calculation:

- Divide the remaining number of lots or tracts to be sold by the annual absorption rate and round up to the next whole number. This is the absorption period, or number of years required to sell the remaining lots or tracts.

- It is important to calculate the sellout percentage first. If the sellout percentage is 80% or greater, present worth procedures do not apply. It is necessary to calculate the absorption rate in order to determine the absorption period.

Consult local developers and real estate professionals for their opinions of the absorption period required for a single competitively isolated tract being sold as a unit or a development without recent sales activity.

Example: Absorption Period Calculation

Approved Subdivision Plat Data Assumptions:

| Approved Subdivision Plat | = 120 lots |

|---|---|

| Original year offered for purchase | = 2000 |

| Total lots sold through the appraisal date | = 95 |

| Total lots sold during data collection period | = 15 |

The absorption period calculation:

| Total number of lots | = 120 lots |

|---|---|

| Total number sold | = 95 |

| Sellout percentage | = 79% (95 ÷ 120) |

| Lots remaining at beginning of data collection period | = 40 |

| Lots sold in the last 18 months* | = 15 |

- 15 ÷ 18 months X 12 months = 10 lots sold per year

- An average of 10 lots sold each year during the 18 months preceding the appraisal date.

- Lots remaining = 25

- 25 ÷ 10 = 2.50 years

From the calculation, it is estimated that it will take 2.50 additional years to sell the remaining 25 lots. Therefore, the absorption period calculated is 3 years. The absorption period is rounded up to the nearest whole number of years to ensure that the period is long enough.

* Beginning of data collection period to appraisal date equals 18 months.

Apply Present Worth Valuation Procedures to Adjusted Selling Price

Vacant Land Valuation Process - PW of $1 Per Period

All vacant lots or tracts are eligible for present worth valuation. In vacant land discounting procedures, present worth value is synonymous with actual value or market value. To determine the discounted present worth value of each subdivided lot within an approved plat or tracts of land within a competitive environment, the following process is used to determine the appropriate "Present Worth of One Dollar Per Period".

- Discount Rate

- Determine the appropriate discount rate using the Weighted Average Cost of Capital, the Summation technique, or market/investor surveys. Discount rates may be rounded to the nearest one-half percent.

- The summation technique used for the current discount rate is shown in Addendum 4-B, Discount Rate Calculation and in the Definition of Terms topic at the end of this chapter.

- Annualized Income

- Determine the absorption period for the remaining lots or tracts within an approved plat or competitive environment. If additional information is needed, refer to the Determine the Absorption Period topic located in a previous part of this chapter.

- The absorption period is calculated as of the appraisal date. Divide the adjusted selling price by the number of years in the absorption period to determine the annualized selling price (ordinary level annuity).

- Compound Interest Rate Tables

- The compound interest tables can be found in the Property Assessment Valuation book published by IAAO. Use the annual tables corresponding to the discount rate that was determined.

- Using the Present Worth of One Dollar Per Period, Column #5 of the tables, go to the factor corresponding to the number of years in the absorption period. The number shown is the appropriate factor to be used in the present worth valuation of all vacant parcels within an approved plat.

- The factor is multiplied by the parcel's annualized adjusted selling price.

- Column #5, Present Worth of One Dollar Per Period, of the compound interest tables, is used when multiple tracts of land within a competitive environment of unplatted properties or subdivided lots within an approved plat qualify for present worth valuation.

- It is also appropriate to use financial calculators or computer programs to run this calculation.

- No Sales Data

- If there are multiple parcels within the approved plat and comparable sales do not exist, the adjusted sales price before discounting is estimated using the procedures described in Chapter 2, Appraisal Process, Economic Areas, and the Approaches to Value, referencing the five accepted valuation methods: sales comparison, extraction/allocation, anticipated use/developmental cost, capitalization of ground rent, and land residual.

Example:

Present Worth Value Calculation Example - Multiple Lots or Tracts

Assume that the adjusted selling price is $10,000, the discount rate is 12 percent, and the absorption period is 10 years.

The actual value is:

| Adjusted selling price | = $10,000 |

|---|---|

| Absorption period | = 10 years |

| Discount rate | = 12% |

| Present Worth of $1 Per Period factor | = 5.650223 |

| $10,000 ÷ 10 yrs = $1,000 (annualized) x 5.650223 | = $5,650 |

The above calculations reflect the present worth of lots or tracts with an adjusted selling price of $10,000 that are expected to sell within ten years from the appraisal date.

Note: Until 80 percent of the lots or tracts in the area are sold, the present worth calculation is made at each change in level of value. The biennial review is necessary since the adjusted sale price, absorption period, and discount rate may change, resulting in a different Present Worth of One Dollar Per Period factor.

Vacant Land Valuation Process - PW of $1

All vacant lots or tracts are eligible for present worth valuation.

Division policy is that the following requirements must be met in order for a tract of land to receive present worth valuation using Column #4, Present Worth of One Dollar, of the compound interest tables.

- The tract is vacant and expected to be sold as a unit.

- There are no similar competing tracts that can be used to establish a competitive environment containing at least two comparable tracts, i.e., the tract is "competitively isolated." Such a tract may be unique due to environmental contamination or government regulations like wetland replacement considerations or zoning restrictions.

- There are no sold tracts comparable to the subject property, thus no competitive environment can be determined.

- It is expected to take more than one year to sell the tract.

- The application of the present worth of one dollar to the adjusted selling price results in a value greater than comparable raw land value. Original land sales, prior to development and just before change in surface use, are collected and verified to determine raw land value on a per unit comparison basis.

The Division is available to assist the county assessor if the situation arises. The present worth of one dollar is never used to value subdivided land.

Present worth valuation using Present Worth of One Dollar, of the compound interest tables is not allowed under the following circumstances:

- Tracts are subdivided into lots within an approved plat.

- Tracts or lots held for open space.

- Tract exists within a defined competitive environment.

To determine the present worth value of each tract, the following process is used to determine the appropriate "Present Worth of One Dollar":

- Discount Rate

- Determine the appropriate discount rate using the Weighted Average Cost of Capital, the Summation technique, or market/investor surveys. Discount rates may be rounded to the nearest one-half percent.

- The summation technique used for the current discount rate is shown in Addendum 4-B, Discount Rate Calculation and in the Definition of Terms at the end of this chapter.

- Estimated Sale Date

- Determine the absorption period for the tract by estimating the number of years to its sale date and rounding to the next whole number. The absorption period is calculated as of the appraisal date.

- If additional information is needed, refer to the Determine the Absorption Period topic located previously in this chapter.

- Compound Interest Table Factor

- Using the compound interest tables, find the set of annual tables corresponding to the discount rate that was determined. Using the Present Worth of One Dollar, Column #4 of the tables, go to the factor corresponding to the number of years in the absorption period. The number shown is the appropriate factor used in the present worth valuation of the single, competitively isolated tract being sold as a unit, and is multiplied times the adjusted, nonannualized selling price.

It is also appropriate to use financial calculators or computer programs to run this calculation.

Note: Present Worth of One Per Period (Column #5), of the compound interest tables is used when multiple tracts of land within a competitive environment, or subdivided lots within an approved plat, qualify for present worth valuation.

- No Sales Data

- If sales do not exist, the adjusted sales price before discounting is estimated using the procedures described in Chapter 2, Appraisal Process, Economic Areas, and the Approaches to Value, referencing the five accepted valuation methods: sales comparison, extraction/allocation, anticipated use/developmental cost, capitalization of ground rent, and land residual.

Example:

Present Worth Value Calculation Example - Column #4 Applied to a Single, Competitively Isolated Tract Being Sold as a Unit

The adjusted selling price is $10,000, the discount rate is 12 percent, and the absorption period is 10 years.

The actual value is:

Adjusted selling price = $10,000

Absorption period = 10 years

Discount rate = 12%

Present worth of One Dollar factor = .321973

$10,000 (nonannualized) x .321973 = $3,220

The calculations reflect the present worth of a single, competitively isolated tract being sold as a unit with an adjusted selling price of $10,000 that is expected to sell ten years (rounded) from the appraisal date.

Developmental Cost Method

The developmental cost method is recommended when sales are inadequate to determine value. The process for this method is similar to the Sales Comparison (Market) Method except for development of the adjusted selling price.

The method can be used in an approved platted subdivision, Planned Unit Development, or with tracts of land within a competitive environment.

The following process is used when valuing vacant land using the developmental cost

approach:

- Identify all lots or tracts within an approved plat or competitive environment.

- Determine the actual value of the raw land before development.

- Determine the adjusted selling price.

- Determine the absorption period.

- Apply present worth valuation procedures to the adjusted selling prices.

Identify all Lots or Tracts Within an Approved Plat

If additional information is needed, refer to Step #1 - Identify All Lots or Tracts Within An Approved Plat earlier in this chapter.

Determining the Actual Value of the Raw Land Before Development

This is necessary for two reasons:

- The Developmental Cost Buildup Method utilizes raw land value.

- To ensure that the present worth value never drops below the actual value of comparable raw, undeveloped vacant land, the raw land value is adjusted to the current appraisal date.

Raw, undeveloped land value is the value of the tract before subdividing, adjusted to the current appraisal date. The actual value of the raw land within an approved plat is determined by consideration of the most comparable raw land sales at the current appraisal date.

Determine the Adjusted Selling Price

Prior to present worth valuation, a percentage of the selling price for each lot or tract is established. When using the "cost buildup" method, the percentage of the selling price is defined as: the raw land value plus the additional value attributable to the direct costs of installed site improvements and other installed improvements such as those for greenbelts and common areas, including landscaping, divided by the total of all direct costs, both incurred and unincurred including raw land.

When using the "cost deduction" method, the direct costs for comparable finished tracts, including raw land, minus the direct costs of site and other improvements not installed, are divided by the total of all direct costs, both incurred and unincurred including raw land. In either case, the percentage is applied to the selling price at the appropriate level of value.

Deductions of indirect costs of development from the selling price are not considered or taken into account, § 39-1-103(14)(b), C.R.S.

The formula to develop the percentage is:

Incurred Direct Development Costs (Including Raw Land) / All Direct Development Costs (Including Raw Land) to Retail Selling Price = Percentage Applied

In the absence of any market sale, retail listing, or comparable sale price, the adjusted sale price is the total of the raw land plus all incurred direct development costs.

In collecting market sales data of raw land and/or finished lots or tracts, contracts for sale are not included as qualified sales unless the transaction is completed, but not formally closed, during the selected data collection period and the sale qualifies as an arm’s length transaction, Platinum Properties Corporation v. Colorado Board of Assessment Appeals, 738 P.2d 34 (Colo. App. 1987). If the terms and conditions of the original agreement have been consummated as evidenced by a deed at some point prior to a review, appeal, or abatement hearing, the transaction is considered as, but is to carry no more weight than, any other sale.

Some developers sell tracts by means of installment land contract sales to generate activity and cash flow. Installment land contracts require little or no down payment and a deed is delivered to the purchaser when specific conditions are met. Installment land contracts are considered in the same manner as sales consummated by deed only when determining the absorption rate.

Developmental Cost Buildup Method

First, the raw land is valued at the current level of value. The value doesn’t include any development costs.

Second, the direct costs associated with the installed site improvements and other installed improvements that are present on the assessment date are determined as of the current appraisal date and added to the raw land value. Other installed improvements include, but are not limited to; greenbelts, landscaping, and common areas. The result is divided by all direct costs of development, both incurred and unincurred including raw land, to obtain a “percent complete” of total land development.

This method of developing a percentage is preferred in the early stages of development if the sales comparison approach has been considered first, but eliminated due to a lack of qualified sales data. Refer to the examples following the description of the Developmental Cost Buildup and Cost Deduction Methods for additional clarification.

Developmental Cost Deduction Method

The method determines a percentage of the selling price by:

- Establishing the value of the lot or tract as if ready for a structure to be built on it, (as evidenced by the developer’s retail selling prices of comparable lots or tracts)

- Subtracting all the direct development costs associated with site improvements and other improvements not yet installed on the assessment date.

- Dividing the result by all direct costs of development, both incurred and unincurred including raw land.

In deciding which method to use, the method that requires the least amount of adjustment is usually the most reliable.

Example:

Developmental Cost Buildup Method

Assume that the lots being appraised were developed through the 4th of 6 stages of

development. The calculation of the percentage is as follows:

| Direct Costs | |

|---|---|

| Raw Land Value | $15,000 |

| Survey Costs | + 1,500 |

| Subdivision Approval | + 1,500 |

| Roads/Paving | + 3,000 |

| Water/Utilities | + 6,000 |

| $27,000 |

$27,000 (Incurred Direct Costs) / $36,000 (Total Direct Costs) = Lot is 75 percent complete. (Based only on direct costs, but applied to the total sale price)

Example:

Developmental Cost Deduction Method

Assume that the lot or tract being appraised is developed through the 4th stage of 6 stages of development. The calculation of the percentage is as follows:

| Direct Costs | |

|---|---|

| All Direct Costs, both Incurred and Unincurred Including Raw Land | $36,000 |

| Amenities | - 3,000 (unincurred) |

| Sewer/Drainage | - 6,000 (unincurred) |

| $27,000 |

$27,000 (Incurred Direct Costs) / $36,000 (Total Direct Costs) = Lot is 75 percent complete. (Based only on direct costs, but applied to the total sale price)

As can be seen from the previous two examples, the same percentage of completion is obtained by either the developmental cost buildup method or the developmental cost deduction method.

Physical site improvements may be partially installed as of the assessment date. Appropriate adjustments are made to account for the value of partially installed items.

Lump-sum adjustments are made, but they should be compared to the direct costs of the installed improvements of a completed lot or tract to ensure that no errors exist.

The method selected is applied to all vacant land lots or tracts, whether sold or unsold, within an approved plat. Consideration is given to each lot or tract's location, desirability, physical characteristics, and use.

Determine the Absorption Period

This process is identical to the process used to determine the absorption period under the Sales Comparison Method topic.

Please refer to the Determine the Absorption Period topic under the Sales Comparison Method for the appropriate procedures to be used.

Apply Present Worth Valuation Procedures to Adjusted Selling Price

The process is identical to the process used to apply present worth valuation procedures to the adjusted selling price under the Sales Comparison Method topic.

In the present worth valuation of vacant land, the present worth value of the land is synonymous with actual or market value.

Definition of Terms

Absorption (Sellout) Period

The absorption (sellout) period is the number of years during which vacant land lots or tracts are expected to be sold within an approved plat or competitive environment, or the number of years required to sell a single competitively isolated tract of land as a unit. This time period represents the time necessary to achieve 100% sellout of the approved plat or competitive environment. The period of time is calculated by dividing the number of lots or tracts to be sold by the absorption rate, and then rounding to the next whole number.

In the case of a tract of land being sold as a unit, the estimated number of years to the sale date is rounded to the next whole number. The period is expressed as the whole number of years necessary to sell the vacant lot or tract.

Since one of the present worth criteria requires an absorption period of greater than 12 months from the appraisal date after rounding, the minimum absorption period is two years as of the appraisal date. The minimum absorption period in an intervening year is one year.

For subdivisions formed after the June 30 appraisal date, absorption rates from comparable subdivisions are used to determine the absorption rate.

Use of square foot, as a unit of comparison to measure absorption, is not provided for in the statutes and is not allowed.

Absorption Rate

The absorption rate is the rate at which properties are sold in a given area. The rate is calculated in sales per month and then annualized by multiplying the result by 12.

The period of time used for calculation of the absorption rate is based on the data collection period from the beginning date of the collection period to the appraisal date. If there is insufficient sales history, the absorption rate of a comparable approved plat should be used.

The beginning date for marketing lots or tracts is sometimes used for new developments. If lots in an approved plat begin selling after the beginning of the 18-month data collection period, but before the end of the data collection period, the number of months that the lots or tracts are available for sale is used to calculate the absorption rate.

For subdivisions without sales data, or for those formed after the June 30 appraisal date, absorption rates from comparable subdivisions are used. However, sales that may have occurred after the appraisal date may be used as a check to ensure that the comparable subdivision’s absorption rate is truly comparable.

If no comparable subdivisions exist, at least one sale is assumed to have occurred during the data collection period. For example, for an 18-month sales data collection period the .0555 monthly absorption rate is annualized by multiplying it by 12, which results in a yearly absorption rate of .6666.

The rate divided into the number of lots or tracts remaining to be sold on the appraisal date, when rounded to the next whole number, results in the absorption period used for the approved plat. Use of square foot, as a unit of comparison to measure absorption, is not provided for in the statutes and is not allowed.

Actual Value

Actual value is synonymous with market value. In using the market approach to value vacant land, actual value is the value of the lot or tract after application of present worth valuation procedures. When there is no application of present worth procedures, actual value is the adjusted selling price of comparable sold properties.

Adjusted Selling Price

The adjusted selling price is the selling price of a lot or tract after deducting the value of nonrealty items which are included in the sales price and after application of any market adjustments for cash equivalency (atypical financing), for time, for differing property characteristics, and for those direct costs of development included in the selling price but not installed as of the assessment date. The adjusted selling price is the value subject to present worth valuation procedures.

Anticipated Use or Developmental Cost Methods

A land valuation technique that requires all direct and indirect development costs for installed infrastructure/site improvements and other amenities added (cost buildup method) to the value of the raw land, or all direct and indirect development costs for uninstalled improvements and amenities subtracted (cost deduction method) from the anticipated sales price of developed lots or tracts to indicate the value of a lot or tract.

Appraisal Date

June 30 of the year prior to the year of general reassessment.

Approved Plat

An approved plat is an instrument which, after appropriate approval, is recorded with the clerk and recorder of the county in which the realty is located. Approved plats are defined as:

- For subdivided land, the approved subdivision and/or its approved filings and/or its approved development tracts

- For Planned Unit Developments, the approved plan

Cash Equivalency Adjustment

A cash equivalency adjustment is the required adjustment to the price of a comparable sale to reflect the amount of cash the seller would have received if no special financing terms or other incentive had been given to the buyer. The appraiser must consider and analyze a cash equivalency adjustment when a seller provides a buyer with favorable terms or other incentives. Typically, the seller is compensated for the cost of the incentive by increasing the selling price. This price increase is not real property. Therefore, when estimating actual value, the comparable sale must be adjusted (usually down) for this incentive to represent the normal consideration for the real property as if sold unaffected by special or creative terms. Examples include, but are not limited to, seller carried below-market interest rates and excessive seller-paid closing costs.

Competitive Environment

A competitive environment is defined as a group of unplatted properties that share sufficient similar characteristics considered for purchase by buyers interested in the similar (homogeneous) property characteristics. A competitive environment can be delineated using the homogeneous property characteristics. The likely competition among such properties defines the competitive environment.

Development Costs

A development cost is any cost necessary to bring a complete land development into existence including developer's or subdivider's marketing cost, overhead, and profit. Development costs are either direct or indirect.

Direct Development Costs

A direct development cost is any cost required for the planning, engineering, and physical installation of tangible development improvements or amenities necessary to convert a raw land lot or tract into building sites; including the direct costs of associated greenbelts, common areas, and landscaping.

Examples of direct costs can be found in Step # 5 - Deduct Unincurred Direct Development Costs in the Sale Price.

Unincurred direct costs that are reflected in the selling price of the land, but have not been incurred as of the assessment date, are allowable deductions to establish an adjusted selling price.

Discount

Discount is the conversion of future payments into present value. In vacant land present worth valuation procedures, discounting is necessary to establish the present worth or present actual value of vacant land, as of the appraisal date, within an approved plat, within a competitive environment, or for competitively isolated tracts of land for which present worth valuation is applicable.

Discount Rate

A discount rate is a rate of return on capital used to convert future payments or receipts into present value. In vacant land present worth valuation procedures the discount rate is used, in conjunction with the sellout period, to determine the appropriate present worth factor to apply to an adjusted selling price (ASP).

Discounted Cash Flow Analysis

Discounted cash flow analysis is a procedure in which anticipated future net cash flows are discounted to a net present value by using an appropriate discount rate(s). The procedure is based on the assumption that the benefits received in the future are worth less than benefits received now.

Incurred Costs of Development

Incurred costs of development are direct and indirect costs that have been expended, as of the assessment date, to develop a parcel of land into salable building sites; including associated greenbelts, common areas, and landscaping to sell the sites.

Indirect Development Costs

Indirect development costs are any costs not directly part of the planning, engineering, and installation of tangible development improvements or amenities to land lots or tracts.

Examples of indirect costs can be found in Step # 5 - Deduct Unincurred Direct Development Costs in the Sale Price.

Infrastructure

Infrastructure is a term used to describe utilities, support services, and facilities that are an integral part of an approved plat or competitive environment.

Installment Land Contract

An installment land contract is a contract in which a purchaser of real estate agrees to pay a small portion of the purchase price when the contract is signed and additional sums, at intervals and in amounts specified in the contract, until the total purchase price is paid and the seller delivers the deed. Lots or tracts under installment land contracts are considered sold solely for the purpose of determining absorption calculations.

Level of Value

Level of value is defined as actual or market value as of the June 30 appraisal date.

Market Value

Market value is the most probable price, as of a specified date, in cash, or in terms equivalent to cash, or in other precisely revealed terms, for which the specified property rights should sell after reasonable exposure in a competitive market under all conditions requisite to a fair sale, with the buyer and seller each acting prudently, knowledgeably, and for self-interest, and assuming that neither is under undue duress. The Appraisal of Real Estate, 14th Edition, The Appraisal Institute, Chicago, IL, 2013.

Nonrealty (Nonreal Property) Items

Nonrealty items are items, other than land and improvements, which have value and are reflected in the sales price of a property. Nonrealty items may include, but are not limited to, personal property, trade considerations, unfulfilled contractual agreements, and unassigned development rights. Ad valorem valuation requires that an adjustment for any nonrealty items be made to a confirmed sale prior to further market adjustments for financing, time, and physical characteristics, § 39-1-103(8)(f), C.R.S.

Platted Land

Platted land is land located within an approved plat, plan, or map of a city, town, section, or subdivision that indicates the location and boundaries of individual properties. Platted land does not have to be an approved legal subdivision.

Present Worth

Present worth is the value of a future payment or series of future payments discounted to the current date or to a specified time period.

Present Worth of One Dollar

Present worth of one dollar is a compound interest factor that indicates how much $1 due in the future is worth today.

Present Worth of One Dollar Per Period

Present worth of one dollar per period is a compound interest factor that indicates how much $1 paid periodically is worth today. Also called an ordinary level annuity.

Raw Land

Raw land is the original tract of land prior to development or subdividing, on which neither improvements have been constructed nor any development costs have been incurred.

When determining raw land value, all confirmed arm’s-length sales of undeveloped land, e.g., large tract agricultural land sales, within the data collection period are considered and a representative, defensible market value per unit is established. Entitlements must be considered.

Comparable sales are selected for similarity to the subject tract in size and development potential. It is essential that the sales be time adjusted to the final date of the data-gathering period in order to account for any changes in economic conditions affecting the market value.

In the absence of comparable sales within a county, verified vacant land sales from neighboring counties should be considered with locational adjustments applied if necessary, Board of Assessment Appeals, et al., v. E.E. Sonnenberg & Sons, Inc., 797 P.2d 27 (Colo. 1990).

Raw land is typically measured and appraised on a per acre basis, although it may be apportioned to lots or tracts on a square foot basis when determining whether or not present worth values exceed raw land values.

Realty (Real Property) Items

Realty items are considered to be the real estate and rights of ownership that are transferred at time of sale. Realty is valued for ad valorem purposes.

Retail Selling Price

The retail selling price is the actual or market price paid or expected as of a given date. Retail selling price, unlike sales price, may be calculated as of a future date including all direct and indirect development costs. Retail selling price is sometimes referred to as "asking" price or "offering" price.

Sales Data-Gathering Period

The sales data-gathering period is the amount of time used to gather sufficient information for use in the three approaches to value. This period is proscribed by statute being a minimum of 18 months and a maximum of 60 months. Assessors may use as many preceding six-month periods past the 18-month minimum until sufficient information exists to value properties, up to the 60-month maximum, § 39-1-104(10.2)(d), C.R.S.

Sales (Selling) Price

Sales (selling) price is the price paid for a property or a transfer of property for a fixed price in money or its equivalent. The price is generally indicated by the recorded documentary fee or the TD-1000, Real Property Transfer Declaration. The sales price, however, may include nonrealty items.

Site Improvements

Site improvements are infrastructure improvements to land that enable the owner to develop the property for a more effective purpose than its present use.

Examples of site improvements are streets, curbs and gutters, culverts and other sewage and drainage facilities, utility easements, and utility hookups for individual lots or tracts.

Summation Method for Discount Rate Development

The summation method is a discount rate development technique that combines component rates which are necessary to adequately measure the appropriate return on investment that would be expected by an investor.

The summation method of discount rate development combines four components:

- Safe rate

- Management rate

- Risk rate

- Consideration for illiquidity