Chapter 3 - Specific Assessment Procedures

Introduction

The following procedures and processes are listed in alphabetical order and are intended to provide assessors and their staff with guidelines for specific assessment administrative tasks; modification may be necessary depending on county resources. Chapter 4, Assessment Math, contains more detailed instructions for mathematical procedures such as prorating values and computing tax bills.

Taxable Property

All property, real and personal, located in the state of Colorado on the assessment date, January 1, is taxable unless expressly exempted by the Constitution or state statutes, § 3, art. X, COLO. CONST., and § 39-1-102(16), C.R.S.

Colorado Valuation Procedures

Most property classes in Colorado are valued using the three approaches to value: the market approach, the cost approach, and the income approach. The exceptions to the three approaches include residential real property (market only), agricultural land, and natural resource land (special valuation procedures based on productivity and production).

The market, cost, and income data that county assessors use to apply the appropriate approaches to value is collected during specific periods prescribed by statute and represents a certain “level of value.” Currently, the data collection periods and level of value change every odd numbered year, § 39-1-104(10.2), C.R.S.

Property taxes are not calculated on the “full actual value” as determined by the assessor. Instead, an assessment percentage is applied according to the classification of the property, §§ 39-1-104(1) and 39-1-104.2, C.R.S. For property tax year 2025, residential property is assessed at 7.05% for schools and 6.25% for local governments. For property tax year 2025, most nonresidential property is assessed at 27.0% The exceptions are producing mines and producing oil and gas leaseholds, articles 6 and 7 of title 39, C.R.S.

Specific Administrative Processes

Abatements

Abatement petitions are initiated for a variety of reasons. Most often, abatements are filed by taxpayers for the purpose of reducing a prior year’s tax. The county must act on abatements within six months of filing; therefore, a tracking system is helpful in identifying where an abatement is located in the process. Additional information on abatements can be found in Chapter 5, Taxpayer Administrative Remedies. Petitions for Abatement or Refund of Taxes are available on the Division’s website and are shown in Chapter 9, Form Standards.

Initiating an Abatement

The assessor completes the following steps when processing an abatement petition.

- Verify the legal description, owner of record, and the owner’s mailing address.

NOTE: If a petition is filed by an agent, the agent must have written authorization to represent the owner. - Examine the property record and determine if an error, illegality or overvaluation exists. If the issue is overvaluation, determine if a protest was filed for the assessment year in question. If no protest was filed, an abatement petition can be approved.

NOTE: Clerical errors and illegalities are corrected whether or not a protest was filed. An abatement or refund must not be made based upon the ground of overvaluation of property if a protest was filed and a Notice of Determination was issued. However, a statutory exception to the rule exists for personal property when 1) a Notice of Determination has been mailed to the taxpayer, and 2) the taxpayer did not appeal the assessor’s decision to the county board of equalization, and 3) the county assessor has undertaken an audit of the personal property indicating that a reduction in value is warranted, § 39-10-114(1)(a)(I)(D), C.R.S.- Complete steps 6 through 9 below for petitions on which the assessor recommends denial.

- Complete steps 3 through 9 below for petitions on which the assessor recommends approval in whole or in part.

Determine the assessed value attributable to the value adjustment, if any. The taxpayer or agent may have stated only the actual value on the abatement form. The assessed values need to be on the form for the treasurer to make adjustments.

NOTE: Make sure the appropriate assessment rate is used and value adjustments are applied to the properties. This example is for a residential property in tax year 2025:

Example:

Local Government

Actual Rate Assessed Tax

Original $400,000 6.25% $25,000 $1,507.33

Corrected $385,000 6.25% $24,063 $1,450.84

Abate $ 15,000 6.25% $ 937 $ 56.49School

Actual Rate Assessed Tax

Original $400,000 7.05% $28,200 $ 768.45

Corrected $385,000 7.05% $27,143 $ 739.63

Abate $ 15,000 7.05% $ 1,057 $ 28.82

- Verify the tax area, mill levy, and the amount of tax to be abated.

NOTE: Make sure that the appropriate year’s mill levy is used. - Determine if the tax has been paid and verify the amount of tax on the tax warrant.

- Complete the assessor’s recommendation.

- Attach documentation needed to support the assessor’s recommendation.

NOTE: For overvaluation, the assessor prepares evidence for the abatement hearing in the same manner as for an appeal hearing. - Keep a copy of the petition and all documentation.

- Forward the petition to the board of county commissioners.

Data Control Measures

Abstract (class and subclass) reports should be run on a monthly basis to assist the assessor in catching data input and program calculation errors. The following schedule is suggested as a minimum measure.

January 1: Establishes value base on the assessment date.

May 1: Establishes value base before protest period.

July 1: Establishes value base for the required CBOE report.

July 5: Establishes value base after assessor’s protest period.

NOTE: This is important, as the individual class pages of the abstract reflect values as of this time frame.

August 5: Establishes value base after CBOE appeals decisions.

NOTE: This is important, as the cities and towns and school district pages of the abstract reflect values as of this time frame.

August 25: Provides values for the Abstract of Assessment report, certification of values to entities, qualified share of property tax revenue for schools, and actual values for the Division to estimate the residential assessment rate.

Dec. 10: Provides values for recertification of values to entities.

NOTE: The Division recommends the recertification be completed by December 1.

Run an abstract report before and after installing a computer upgrade or when going through a system conversion.

Counties that use the alternate protest and appeals process will modify the above schedule.

The current report should be compared to the prior report. Figures that seem out of line should be verified and corrected if necessary.

After the Abstract of Assessment report has been filed, value changes should be tracked. With this tracking method, the assessor will be able to balance back to the prior report.

The following items are examples of situations to verify:

- Internal codes that are not tied to a subclass code established by the Administrator.

- Classification code with zero value.

- Vacant land classification code with improvement code.

- Exempt classification code with taxable code.

- Mismatched classification codes.

- Improvement classification code with no land code.

- Inordinately large or small values for the class.

- Significant increase or decrease in the number of parcels within a classification (compared to prior year).

- Within a subclass, parcel unit count higher than the improvement count.

- Land value higher than improvement value.

- Zero parcel/unit count for a subclass with a value entry.

- Omission of entire class or subclass (compared to prior year).

- Value entries are rounded to the nearest $10.

- Acreages are rounded to the nearest whole number.

- Proper entry of new construction and destroyed property.

- Proper entry of CBOE adjustments (including the number of adjustments and the value change).

- Verify that the school districts and cities and towns listed in the automated abstract are correct. (If changes occurred, contact the Division.)

- Cities and Towns page must reflect CBOE adjustments.

- School District page must reflect CBOE adjustments.

Actual Value Adjustments For Residential Property

Beginning in 2026, residential properties will receive an actual value adjustment prior to calculating the assessed value for local governments, § 39-1-104.2, C.R.S.

In 2026, the actual value adjustment is 10% of the first $700,000, with an assessed value floor of $1,000. The assessed value floor applies to the total residential parcel value.

Beginning in 2027, the $700,000 threshold will be adjusted to account for inflation in every revalue year. The updated value will be available on the Division of Property Taxation website.

The actual value adjustment is to be applied to every residential parcel classified as such on January 1, the assessment date.

For mixed-use property, with residential and commercial improvements, only the residential portion of the property should receive the adjustment. The value adjustment, 10% of the first $700,000, is applied to the residential portion of the parcel value.

The residential actual value adjustment applies only when calculating the local government assessed value. The school assessed value is calculated from the total, non-adjusted, actual property value.

Great Outdoors Colorado Trust Fund

Each year during the regular tax assessment period, the board of county commissioners of each county in which a state agency has acquired real property shall provide to each state agency that holds such real property interests with the following information, § 33-60-104.5(3)(b), C.R.S:

- The current assessed value of each real property interest expressed in dollars;

- The amount of the payment in lieu of taxes (PILT) due on each real property interest, based on the value and tax rate that would be applicable to the real property interest if it were taxable;

- The date the payment in lieu of taxes is due for such real property interests, based on the date property taxes are due.

Growth Valuation for Assessment

Qualifying counties severely impacted by residential growth may opt to assess new construction that occurs between January 1 and July 1, § 39-5-132, C.R.S. If the county commissioners make a finding of severe growth impact as provided in § 39-5-132, C.R.S., the assessor values new construction on both January 1 and July 1. The prorated value of the construction completed between January 1 and July 1 is added to the assessment roll. If the building is complete on July 1, the value of the construction that occurred between January 1 and July 1 is prorated according to the number of months of the year the building was complete. If the building is not complete on July 1, the value added shall be one-half the difference between the assessed value of the building on January 1 and the assessed value on July 1, § 39-5-132(2)(a)(I)(B), C.R.S.

The classification of the land is based on its status on the January 1 assessment date, which is typically vacant land, unless the newly constructed building is a residential unit. If the newly constructed building is a residential unit and if the land was classified as vacant, the land is reclassified as residential and the assessment rate applied to the land is based on the residential classification, § 39-5-132(2)(c), C.R.S. ARL Volume 3, Real Property Valuation Manual, Chapter 4, Valuation of Vacant Land Present Worth, provides procedures for present worth valuation. In the procedures, it directs that the present worth value is applied only to vacant land. Once a building is on the land, present worth valuation does not apply; thus, the Division suggests the present worth valuation be removed when the land classification is changed to residential due to the installation of a residential improvement.

Taxpayers must be mailed a notice of actual valuation that provides the January 1 value, the prorated valuation of the building, and the total valuation for the entire year. Protests will be heard the following May, at which time the owner can address both valuations, § 39-5-132(2)(a)(I)(C), C.R.S.

A special report must be filed with the county commissioners by August 25 of each year showing the amount of growth for that year, § 39-5-132(3), C.R.S.

Local Government Reimbursement

Local governmental entity means a governmental entity authorized by law to impose ad valorem taxes on taxable property located within its territorial limits; except that the term excludes school districts, § 39-1-104.2(1)(a.5), C.R.S.

Section 39-3-211, C.R.S., requires each assessor to calculate the decrease, if any, in the total assessed value of real property for each local governmental entity between the property tax year commencing on January 1, 2024, and the property tax year commencing on January 1, 2025, due to HB24B-1001.. The assessor shall determine each local governmental entity’s mill levy for the property tax year commencing on January 1, 2024, excluding any mills levied to provide for the payment of bonds and interest thereon, or for the payment of any other contractual obligations approved by the voters.

No later than March 1, 2026, assessors shall report the local governmental entities that had a decrease in assessed value of real property between property tax year 2024 and property tax year 2025. The Administrator may require an assessor to provide additional information as necessary to evaluate the accuracy of the amounts reported, in terms of assessed value, mill levies and revenue. The Administrator shall confirm that the amounts reported are correct, or rectify the amounts if necessary.

The Administrator shall then forward the correct amounts, for a county, to the state treasurer to enable the state treasurer to issue a reimbursement warrant to the county treasurer. If there is insufficient money in the fund for the State Treasurer to issue warrants, the amounts of the warrants will be proportionally reduced.

Manufactured Homes

Terminology

Manufactured Home

Built to Department of Housing and Urban Development (HUD) standards, manufactured homes are typically placed on a temporary foundation and titled. Manufactured homes can also be placed on a permanent foundation and never titled. Titled manufactured homes may or may not have the axles and wheels in place. For structural reasons, the I-beams must be left in place, even if the home is placed on a permanent foundation. Manufactured homes have a red HUD plate on the left rear side of each section.

Definitions.

(7.8) “Manufactured home” means any preconstructed building unit or combination of preconstructed building units that: (a) includes electrical, mechanical, or plumbing services that are fabricated, formed, or assembled at a location other than the residential site of the completed home; (b) is designed and used for residential occupancy in either temporary or permanent locations; (c) is constructed in compliance with the “National Manufactured Housing Construction and Safety Standards Act of 1974”, 42 U.S.C. sec. 5401 et seq., as amended; (d) does not have motive power; (e) is not licensed as a vehicle; and (f) is eligible for a certificate of title pursuant to part 1 of article 29 of title 38, C.R.S.

§ 39-1-102, C.R.S.

Mobile Home

Many mobile homes that were built to American National Standards Institute (ANSI) standards are typically placed on a temporary foundation and titled. Manufacturers stopped making mobile homes in 1976. Mobile homes typically have no label; however, the state of Colorado had a Mobile Home Certificate label for homes built from 1971-1976, and the label was placed on the left rear side of the home.

Definitions.

(8) “Mobile home” means a manufactured home built prior to the adoption of the “National Manufactured Housing Construction and Safety Standards Act of 1974”, 42 U.S.C. sec. 5401 et seq., as amended.

§ 39-1-102, C.R.S.

Trailer House

This is another term for mobile home.

Modular Home

Modular homes are factory built to standards set by International Residential Code (IRC), and International Building Code (IBC) for non-residential property. Prior to 2003, the standards were set by Uniform Building Code (UBC). Modular homes are typically placed on a permanent foundation and not titled. I-beams may be used during transport for support; however, they are removed when the homes are set. Modular homes are identified by a silver plate located under the kitchen sink.

Definitions.

(8.3) “Modular home” means any preconstructed factory-built building that: (a) is ineligible for a certificate of title pursuant to part 1 of article 29 of title 38, C.R.S.; (b) is not constructed in compliance with the “National Manufactured Housing Construction and Safety Standards Act of 1974”, 42 U.S.C. sec. 5401 et seq., as amended; and (c) is constructed in compliance with building codes adopted by the division of housing in the department of local affairs.

§ 39-1-102, C.R.S.

Factory Built Home

This is another term for modular home.

Panelized Home

Panelized homes are modular homes consisting of packaged components that are assembled on site. They are also built to IRC/IBC/UBC standards.

Camper Trailer

Camper trailers are wheeled vehicles without motive power that are designed to be drawn by motor vehicles over public highways. They are used for temporary living or sleeping accommodations. Camper trailers may have a Recreation Vehicle Industry Association (RVIA) sticker designating them as recreational vehicles and is located inside the door to the trailer. A camper trailer generally has a license plate issued to the owner by county motor vehicle. Multipurpose trailers and trailer coaches are also considered temporary living or sleeping accommodations.

Park Model

Park models are considered recreational vehicles by the Division of Housing. They may have an RVIA sticker designating them as recreational vehicles. Some manufacturers construct park models to IRC standards and place the factory-built plate under the kitchen sink. Other manufacturers construct manufactured homes built to HUD standards that resemble park models.

Sale of New or Used

The seller is responsible for making sure that all property taxes have been paid on a titled manufactured home. When an application for a Certificate of Title is submitted to the State Division of Motor Vehicle by the new owner, it shall be accompanied by an Authentication of Paid Ad Valorem Taxes, also called Authentication/Certification – Manufactured Home Tax, (authentication form) issued by the county treasurer. The manufactured home authentication form is available on the Division’s website at the Forms Index web page and is shown in Chapter 9, Form Standards.

The authentication form indicates that no property taxes for previous years are due on the titled manufactured home. The seller of a titled manufactured home must provide the buyer with a Certificate of Title to facilitate the transfer of the title. The seller must also provide a listing of the household furnishings included in the sale price, §§ 38-29-106, and 107, 39-5-203(3)(a), C.R.S. The seller or the purchaser must file a Manufactured Home Transfer Declaration(MHTD) with the county clerk and recorder, § 39-14-103, C.R.S.

The buyer must apply for a new title from the authorized agent of the county (county clerk or motor vehicle division) within 45 days of the sale of a new manufactured home or within 30 days of the sale of a used home. The authentication form is given to the clerk along with the application for title. The application must be filed in the county where the titled manufactured home is located, and must show the applicant’s source of title and the new or resale price of the manufactured home. It is the responsibility of the buyer to notify the county assessor where the titled manufactured home will be located, the new address, and transfer of ownership, §§ 38-29-108(1) and 38-29-112(1), C.R.S. If the buyer or the seller does not file the Manufactured Home Transfer Declaration, the assessor shall notify either the buyer or seller, §39-14-103(1)(b)(II), C.R.S.

Upon the sale or transfer to a dealer of a manufactured home for which a title has been issued, the dealer is not required to transfer the title of the manufactured home into the dealer’s name as long as the home remains in the dealer’s inventory for sale and for no other purpose, § 38-29-115, C.R.S.

Manufactured Home Transfer Declaration

When a titled manufactured home is conveyed, a completed Manufactured Home Transfer Declaration (MHTD) must accompany the application for new title, § 39-14-103(1)(a), C.R.S. The clerk and recorder does not record the MHTD. The clerk transmits the declaration to the county assessor. The MHTD is a resource for assessors’ in the sales confirmation process that contains valuable information about the sale or transfer of a titled manufactured home.

If a MHTD does not accompany an application for Certificate of Title, the county clerk and recorder shall notify the county assessor that the MHTD was not provided. Upon receiving notice that the MHTD was not filed, the assessor shall send a written notice to the buyer or seller that the MHTD must be filed with the county assessor within 30 days or a penalty of $25 or 0.025% of the sales price, whichever is greater, may be imposed annually until the MHTD is submitted or the home is subsequently conveyed. The Manufactured Home Transfer Declaration is available on the Division’s website and is shown in Chapter 9, Forms Standards.

NOTE: The Real Property Transfer Declaration (TD-1000) is used for real property, including manufactured homes that are permanently affixed to the land and transferred by deed.

Permanently Affixed to the Ground

Certificate of Permanent Location for a Manufactured Home

The owner of a titled manufactured home must file for recording a Certificate of Permanent Location for a Manufactured Home (Certificate of Permanent Location) when the home becomes permanently affixed to an existing site, or it is transported to a site and is permanently affixed to the ground so that it is no longer capable of being drawn over the public highways, and shall present a Certificate of Title together with an application to purge the title from the records manufactured home, the Certificate of Permanent Location must include a copy of the bill of sale and the Manufacturer’s Certificate or Statement of Origin. The titled manufactured home then legally becomes real property, §§ 38-29-112(1.5) and 38-29-202, C.R.S. This means, among other things, that the classification of the manufactured home will change, future transfers of the property will be by deed, and that if property taxes are not paid, a treasurer’s deed cannot be issued for at least three years from the date of the sale of the tax lien certificate. The manufactured home that has a Colorado Certificate of Title shall be valued and taxed separately from the land until the titled manufactured home is permanently affixed to the ground so that it is no longer capable of being drawn over the public highways, § 38-29-112(1.5), C.R.S.

The Certificate of Permanent Location includes items such as: identification of the manufactured home, the legal description of the real property to which the manufactured home has been permanently affixed, verification that the manufactured home is on a permanent foundation, a consent statement by the lien holders(s) if the home is financed, etc. § 38-29-202(2), C.R.S.

Certificate of Permanent Location for a Manufactured Home Subject to a Long-Term Land Lease

Effective July 1, 2009, the owner(s) of a titled manufactured home must file a Certificate of Permanent Location for a Manufactured Home Subject to a Long-Term Land Lease (Certificate of Permanent Location, LTL) when the home is permanently affixed (no longer capable of being drawn over the public highways) to land that is subject to a long-term lease of at least 10 years. For a manufactured home that is titled, the Certificate of Permanent Location, LTL must include an application to purge the Certificate of Title. For a new manufactured home, the Certificate of Permanent Location, LTL must include a copy of the Bill of Sale and the Manufacturer’s Certificate or Statement of Origin.

By signing the Certificate of Permanent Location, LTL, the owner(s) of the manufactured home and the owner(s) of the land subject to the long-term lease consent to the affixation of the manufactured home to the land. The owner(s) of the land and the owner(s) of the manufactured home also acknowledge that the home becomes part of the real property after it is permanently affixed and that, upon termination of the long-term land lease, the ownership of the manufactured home reverts back to the homeowner(s), § 38-29-202(2)(l.5), C.R.S. Both the Certificate of Permanent Location for a Manufactured Home and the Certificate of Permanent Location for a Manufactured Home Subject to a Long-Term Land Lease are available on the Division’s website and are shown in Chapter 9, Forms Standards.

The Division recommends that the assessor physically inspect the manufactured home to verify that the home is on a permanent foundation. Permanent foundation is not defined in statute or by the Division. The Division of Housing generally defines a permanent foundation as a single system for home support and anchoring to the ground. Manufactured homes installed on a permanent foundation must be in accordance with local jurisdictional requirements. An authorized agent must inspect the manufactured home prior to the recordation of the Certificate of Permanent Location.

The State Division of Motor Vehicle will notify the owner and county motor vehicle that the manufactured home Certificate of Title has been purged for ad valorem prior to recording the Certificate of Permanent Location. The assessor will be notified by the county clerk when the Certificate of Permanent Location has been recorded. The home is assessed as a titled manufactured home (1235) for the current year. The following January 1, the land and the manufactured home are listed on one schedule and classified as a single family residence (1112/1212).

Although the statute does not directly address the issue of ownership, legal theory suggests that without other documentation properly establishing a separate ownership (Certificate of Title), the manufactured home becomes attached to, a part of and an appurtenance to the land and the two interests, land and manufactured home, are merged into a single ownership, that of the land. Thus, the assessor should list the land and building as a single ownership.

The purchaser of a new manufactured home that is transported to a site and permanently affixed to the ground so that it is no longer capable of being drawn over the public highways is required to obtain a Certificate of Permanent Location. The owner of the manufactured home shall record the Certificate of Permanent Location along with the Manufacturer’s Certificate or Statement of Origin or its equivalent with the county clerk and recorder and the manufactured home becomes real property when permanently affixed, § 38-29-114(2), C.R.S. The manufactured home is treated as other real property improvements; thus, the home is not assessed until the following January 1. The home and land are listed on one schedule and classified as a single-family residence/land (1112/1212) the following January 1.

Some titled manufactured home owners whose homes are permanently affixed to the ground refuse to surrender their titles for purging from the records because of urging from mortgage holders or personal convictions. These titled manufactured homes are taxed and valued separately from the land until the owner files an application for purging the Certificate of Title and records a Certificate of Permanent Location. If an owner states that the home is on a permanent foundation but has no proof that the title was purged prior to July 1, 2008, the owner can provide an Affidavit of Real Property for a Manufactured Home. The affidavit must include: a statement acknowledging that the home is permanently affixed, a statement from the county assessor that the home has been valued together with the land, a statement from the county treasurer that taxes have been paid on the manufactured home and land together, and proof that no Certificate of Title exists for the manufactured home, § 38-29-208, C.R.S. The Affidavit of Real Property for a Manufactured Home is available on the Division’s website and is shown in Chapter 9, Forms Standards.

Manufactured Home Movement

Existing Homes

The owner of a titled manufactured home has the responsibility of notifying both the county assessor and the county treasurer before moving the home. “Owner” means the owner at the time of the change of location, §§ 38-29-143(1), 39-5-204(1)(a), and 39-5-205, C.R.S.

The assessed value of a titled manufactured home is prorated whenever the manufactured home moves out of or into the state, if the manufactured home becomes the property (inventory) of a dealership if it is located on the dealer’s sales display lot, or if it is sold by a dealer, §§ 39-5-204(1)(c)(II) and 39-5-203(3)(a), C.R.S.

The assessor does not prorate the value if the move is intra-county (within the county) or if the home moves to another Colorado county. If the home is moved within the county, the tax area code is assigned based on the on the location January 1 and will remain on the property for the entire year. January 1 of the following year, the tax area code will need updating to match the new location. A flag in the system may assist in tracking these changes. If the home is moved to another county, upon notification to the treasurer, the taxes become due and payable to the county where the home was located on January 1, § 39-5-205(3)(a), C.R.S.

Upon receiving notification of a home that leaves the state, the assessor prorates the value of the titled manufactured home for the time, in full months, it was in the county. If the home was in the county on the 16th day or later, a full month is counted. If it leaves the state before the 16th, that month is disregarded, § 39-5-205(3)(b), C.R.S. The taxes must be paid prior to the home moving out of the county.

An authentication form is completed when the ownership of a titled manufactured home changes or when a titled manufactured home will be moved. The authentication form shows information such as the current location, future location, value proration, and taxes due, if any. When a titled manufactured home move is intra-county, the “no proration necessary” box on the authentication form is checked. The taxes become due and payable the following January 1 for intra-county moves. When the titled manufactured home moves to another county in Colorado, the value is not prorated; the county treasurer collects the full year’s taxes prior to the move.

When a titled manufactured home is brought into a county from out of state after the assessment date, the titled manufactured home owner must notify the county assessor and the county treasurer, within 20 days, of the location of the manufactured home and the mailing address of the owner. The county assessor must determine the market value of the manufactured home and prorate such value for the amount of time, in full months, remaining in the year. If the titled manufactured home is brought into the state on or after the 16th of the month, that month is disregarded, §§ 38-29-143(1) and 39-5-204(1)(c)(II), C.R.S. If the home is moved from another Colorado county, the home is not assessed until the following January 1 because the home was taxed by the previous county for the full year, § 39-5-205(3)(a), C.R.S.

Refer to Chapter 4, Assessment Math, for proration calculation rules and examples. The prorated value must remain on the assessment roll and is not removed until the tax warrant has been produced.

If the current year’s mill levy has not been set, the prior year’s mill levy should be used in calculating the amount of tax due. When the mill levy for the current year has been set, the prorated taxes on titled manufactured homes that have moved out of the state are recalculated by the treasurer. The treasurer refunds overpayment of taxes after the tax warrant has been produced. Refunds are usually handled through the abatement process. Underpayment of taxes is considered an erroneous assessment by the treasurer and reported with other erroneous assessments as required by law, §§ 39-5-205, 39-10-114(1)(a)(I)(A), and 39-11-107, C.R.S.

When a titled manufactured home is moved from the state, the county treasurer collects the taxes based on the prorated value for the year. The amount of tax paid is shown on the authentication form, § 42-4-510(2)(a), C.R.S. The Authentication/Certification – Manufactured Home Tax form is shown in Chapter 9, Forms Standards.

Existing Homes on Permanent Foundation

The owner of a manufactured home that has been permanently affixed to the land must record a Certificate of Removal prior to movement from its permanent location, § 38-29-203, C.R.S. The Certificate of Removal for a Manufactured Home is available on the Division’s website and is shown in Chapter 9, Forms Standards. However, if a Certificate of Permanent Location was not previously recorded, the owner must record an Affidavit for Real Property for a Manufactured Home along with the Certificate of Removal, §§ 38-29-202 and 208, C.R.S. In order to obtain a Certificate of Title, the owner must provide an application for title, a statement that the identification number has been verified pursuant to § 38-29-122(3)(a), C.R.S., and copies of all conveyance documents affecting the home from the date the home was affixed to the ground. In cases where a manufactured home occupies real property subject to a long-term land lease of at least ten years, a copy of the long-term land lease must be supplied in addition to the above documents. The county clerk will accept these documents as sufficient evidence of the applicant’s proof of ownership of the manufactured home, § 38-29-107, C.R.S.

New Homes

When a new titled manufactured home is sold to a consumer, there are no property taxes immediately due and payable on such home. It was part of the inventory of a dealer or manufacturer, and inventories held primarily for sale are exempt from property taxation. Therefore, neither an Authentication of Paid Ad Valorem Taxes nor a Transportable Manufactured Home Permit from the county treasurer is required to move a new titled manufactured home. Because of this, assessors may not receive notice of every new titled manufactured home that moved into their counties, § 42-4-510(2)(a), C.R.S.

Many manufactured home dealers have their own vehicles for moving the homes they sell. Such dealers usually apply for an annual moving permit. This means there are no single trip permits that provide a record of individual moves. If neither the dealer nor the purchaser of a new home notifies the assessor of the move, the home may not be valued for the assessment year in which it sold. To prevent this from happening, assessors may inspect the records of moving permit holders. Section 42-4-510(2)(b)(II), C.R.S., states the following:

Permits for excess size and weight and for manufactured homes.

(2)(b)(II) Holders of permits shall keep and maintain, for not less than three calendar years, records of all manufactured homes moved in whole or in part within this state, which records shall include the plate number of the towing vehicle; the year, make, serial number, and size of the unit moved, together with the date of the move; the place of pickup; and the exact address of the final destination and the county of final destination and the name and address of the landowner of the final destination. These records shall be available upon request within this state for inspection by the state of Colorado or any of its ad valorem taxing governmental subdivisions.

§ 42-4-510, C.R.S.

Required Permits

The treasurer issues a Transportable Manufactured Home Permit for every titled manufactured home that is moved. The Transportable Manufactured Home Permit is valid for 30 days and for a single trip. The treasurer may charge up to $10 for the permit. The permit is six by eleven inches, printed on a fluorescent orange card, and must be visible during the move, § 42-4-510(2)(a), C.R.S. If the move is within a county or to an adjoining county on county roads, the authentication form serves as the moving permit.

If the move is on state highways, the owner or mover must obtain an excess size transport permit from the Colorado Department of Transportation (CDOT). This permit must be affixed to the manufactured home. Before CDOT will issue the permit, the owner must have an authentication form and a Transportable Manufactured Home Permit issued by the treasurer, § 42-4-510(2)(b), C.R.S. Movers of manufactured homes may apply for a single trip, special, or an annual permit.

Penalties

If the owner fails to notify the county assessor and treasurer of the location change of a titled manufactured home, the owner is guilty of a misdemeanor traffic offense and, upon conviction, shall be punished by a fine of not less than $100 nor more than $1,000, § 38-29-143(2), C.R.S.

The fine for the movement of a titled manufactured home without a permit or a prorated tax receipt and a Transportable Manufactured Home Permit is $200, § 42-4-510(12)(b), C.R.S.

The district attorney shall investigate and prosecute any allegations that a titled manufactured home has been moved without a valid permit. The allegations may be made by any law enforcement official or any employee of a county assessor’s or treasurer’s office, § 42-4-510(10), C.R.S.

Proof of Manufactured Home Identification

In order to obtain specific information regarding a titled manufactured home, an inspector verifies the following: the identification number, the make and year of the manufactured home, and additional information that may be required by the clerk and recorder. The inspector may charge a fee for the inspection; however, the fee shall not exceed a reasonable cost related to the inspection and the inspector must notify the owner of the fee prior to inspection. If the inspector determines that the identification number has been destroyed, the owner must request that the county clerk assign a distinguishing number to the titled manufactured home. The new assigned number must be affixed to the manufactured home in a door frame or fuse box or as determined by the county clerk. A manufactured home inspector may be designated by the county clerk. A Colorado law enforcement officer, a person registered to sell manufactured homes, or a county assessor may be designated as an inspector, §§ 38-29-122 and 123, C.R.S.

Manufactured Home Destroyed

When a titled manufactured home is destroyed, dismantled, sold as salvage, or otherwise disposed of, the owner of the manufactured home, or the owner of the land upon which it is located, must file for recording a Certificate of Destruction for a Manufactured Home with the clerk and recorder of the county where the home is located, § 38-29-204, C.R.S. A completed form shall include a verification that the home has been destroyed and the consent or release of all holders of liens and mortgages or proof that their consent or release was requested and no response was received within 30 days.

NOTE: If the manufactured home was destroyed by a natural cause as defined in § 39-1-102(8.4), C.R.S., please follow the procedures for destroyed property in Chapter 4, Assessment Math.

The Certificate of Destruction must be accompanied by a Certificate of Taxes Due or an Authentication of Paid Ad Valorem Taxes issued by the county treasurer. If a Certificate of Title was issued that has not been purged, the Certificate of Destruction must also be accompanied by an application to cancel the Certificate of Title.

However, if a governmental entity has deemed the manufactured home to be materially dangerous or hazardous pursuant to local building or health codes, the owner of the land upon which the manufactured home is located may file and record a Certificate of Destruction without attaching a Certificate of Taxes Due or an Authentication of Paid Ad Valorem Taxes and without filing an application to cancel a Certificate of Title. The Certificate of Destruction must be accompanied by evidence of the violation of building or health codes.

The Certificate of Destruction for a Manufactured Home is available on the Division’s website and is shown in Chapter 9, Form Standards.

Held as Inventory

Manufactured homes located on sales display lots of manufactured home dealers and listed as inventory of merchandise by such dealers are exempt from property taxation, § 39-5-203(3)(a), C.R.S. Titled manufactured homes taken in trade or purchased by dealers and which remain on locations other than the dealer’s sales display lot are taxable. New or used manufactured homes owned by the dealer, which are situated on locations other than the dealer’s sales display lot are taxable. The value is prorated by the day, based on the date the home changed taxable status.

A Special Notice of Valuation should be sent to a taxpayer when a titled manufactured home loses exempt status because it is moved out of dealer inventory or off the sales display lot.

Soldiers’ and Sailors’ Civil Relief Act – Exemption

A federal law, known as the Soldiers’ and Sailors’ Civil Relief Act of 1940, prohibits the taxation of personal property, except that used in a trade or business, owned by United States military personnel who are not legal residents of the state, and who are absent from their home states and stationed in another state solely by reason of military orders. The exemption is applicable to titled manufactured homes that are owned by such military personnel and that are not permanently affixed to the land on which they are located.

Assessors of counties wherein such titled manufactured homes are located should have on file a statement by all military persons owning such homes that they are the owner, they use the home as their residence while stationed in Colorado, and they are not a legal resident of Colorado. The statement should also be signed by the appropriate military officer of the base, such as the judge advocate or commanding officer.

Non-residential Use

Manufactured homes with a non-residential use are classified according to their use and the corresponding assessment rate is applied to the actual value. An example of this is a manufactured home used as a sales office.

Camper Trailers, Multipurpose Trailers, and Trailer Coaches

Camper trailers, multipurpose trailers, and trailer coaches are categorized as Class D vehicles, and are issued plates by the county clerk of the county in which the owner resides. The controversy occurs when these types of trailers are parked in one place for an extended period of time. For definitions and classification guidelines, see Chapter 6, Property Classification Guidelines and Assessment Percentages.

Exemption

Commencing January 1, 2022, a titled mobile home or manufactured home with an actual value of $28,000 or less is exempt from the levy and collection of property taxation, §39-3-126.5(3), C.R.S.

Mapping Processes

Processing Plats

Subdivision and condominium plats can be processed at any time during the year. The original parcel value and classification must remain the same as assigned to the property on the January 1 assessment date.

Make one copy of the plat for the appraisal file and one copy for the mapping file. (Mapping section)

- Appraisal file (all pages).

- Mapping file (first page only for condo plats).

NOTE: See Subdivision, Townhome, Condominium, and PUD Plats for map maintenance.

Review the plat for the following:

- Verify the subdivided property by confirming the legal description and acreage.

- Verify ownership - does the owner listed on the plat match the owner listed on the ownership record and declaration? IT MUST!

- Verify that the owner(s) signed the plat and that it has been acknowledged.

If the plat is not signed by the owner(s), contact the planning department or owner of record and find out why.

- For resubdivision plats, determine when the original subdivision was processed.

- If the original subdivision was processed prior to the current assessment date, proceed with step 4.

- If the original subdivision was processed after the current assessment date, refer to Resubdivision Plats – Processing, following this section for processing procedures.

- Determine if the roads are dedicated to the county or city and accepted for public use. (Applies to subdivision plats.) This information is generally located in the dedication statement on the plat.

- Roads that are dedicated and accepted by the county or city are exempt from taxation.

- Roads that are not dedicated and accepted are taxable and should be listed under the property owner’s name and classified as 0100 or 0200.

- Is the common area owned by a conforming common interest and ownership community? (Applies to subdivisions.) Refer to ARL Volume 3, Real Property Valuation Manual, Chapter 7, Special Issues in Valuation.

- If so, the value of the common area should be reflected in the value of the individual subdivision lots and the common area should not be separately assessed. The common area should be assigned a parcel or schedule number and also be flagged with a code that prevents NOVs and tax bills from being processed for these common area accounts.

- If not, the common area should be valued separately and carried under the property owner’s name, usually the homeowner’s association.

For condominiums, review the declaration for the following:

- Verify the unit numbers on the declaration along with the percentage of general common elements per unit. Total the percentages; they must equal 100 percent. If the plat information differs from the declaration, contact the planning department or owner of record and find out why.

- Check for garage or parking space units. Should they have separate appraisal records or are they a part of the common elements?

- Verify how the units are owned. (Time share or quarter share, unit numbers or letters, building number or letters, name of the project, garage and parking spaces, etc.)

A condominium project cannot be processed without a declaration. Watch for missing exhibits listed in the declaration.

- Create a master (recap) card for the condominium, townhouse, or PUD project. Areas to complete:

- City or town.

- Notation of the original legal including lot, block and subdivision could be helpful.

- Name of the project.

- Owner’s name and address, date of the plat and declaration, and reception numbers.

- Important remarks concerning the project, such as time share or quarter share, percent complete, date project started, number of buildings, number of units, etc.

- File a cross-reference card showing the name of the project, the date and reception number of the plat and declaration, etc. under the original legal description. This could avoid unnecessary delays in locating information.

- Obtain parcel identification numbers from the mapping section for each lot, unit, and common area.

Determine the actual and assessed values for land and improvements.

WHEN PROCESSING PLATS, REMEMBER: Total parcel values are set as of the property status on the assessment date and cannot be increased for the year the plat is filed. The account(s) must be flagged for a value adjustment the following year. Abstract codes are assigned based on the use of the property on the assessment date. The codes are changed the following year.

- If a project is broken out before the notice of valuation deadline, the current land and improvement values should be verified with the Appraisal Team.

NOTE: This check is suggested because the current actual value as of the assessment date may not be listed on the assessment record at the time of processing. - If a project is 100 percent complete on January 1, but the plat for the project was not filed by the completion date, the land and improvement value should be verified with the Appraisal Team.

If a project is broken out after the notice of valuation deadline, the current actual value as of the assessment date is apportioned to the lots or units in the project.

This apportionment can be based on acreage, buildable units, site, or the percentage a unit has in the general common elements. The method used should be verified with the Appraisal Team.

- If a project is broken out before the notice of valuation deadline, the current land and improvement values should be verified with the Appraisal Team.

- Set up appraisal records for each lot, unit, road, common area, and garage units when applicable. Include the following:

- Schedule or parcel number, tax area, abstract classification code(s), name of project or subdivision, building and unit number or the block and lot number.

- Name of the current owner, date of the subdivision or condominium plat, condominium declaration, and reception numbers.

- Condominiums: The interest percentage in the general common elements attributable to each unit as outlined in the declaration.

- Subdivisions, townhomes, and PUD: Acreage of the lot and number of buildable units, if provided.

- Land and improvement actual value.

- Enter new numbers into the computer system. Be sure to deactivate old numbers.

- Set up the necessary subdivision files.

For additional information on the subdivision approval process, refer to your county planning and zoning guidelines and procedures.

Resubdivision Plats – Processing

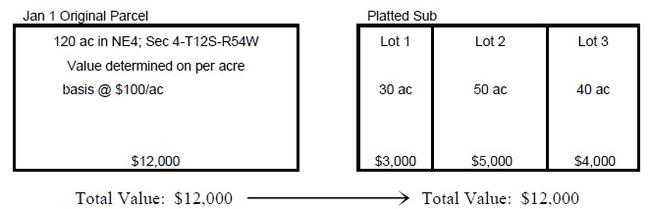

Resubdivision plats can be processed at any time during the year, but the original parcel value and classification must remain the same as assigned on the January 1 assessment date.

When the original subdivision is platted and the plat is recorded at the clerk and recorder’s office, the legal description changes from a rectangular survey or a metes and bounds description to lots and blocks of a recorded subdivision. That legal description change and the allocation of the original parcel value are covered in the general policy as shown below:

When an area is replatted, the total value of the new parcels must equal the total value of the platted parcels. The new accounts must be flagged to be reviewed the following January 1 for classification and valuation adjustments.

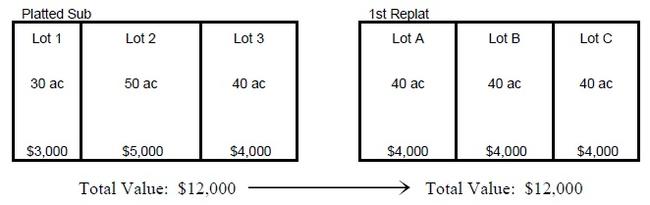

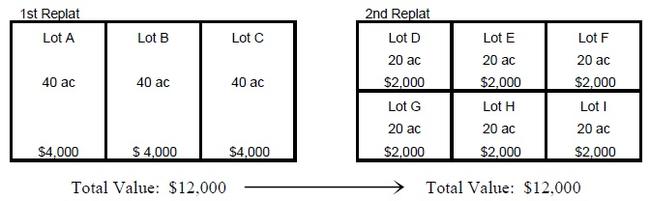

If the replatted lots are further subdivided by a 2nd replat, the total value of the new parcels must equal the total value of the parcels in the 1st replat. Again, the new accounts must be flagged to be reviewed the following January 1 for classification and value adjustments.

This is a simplified example of allocation of value for replatted subdivisions of vacant land. Each subdivision and replat is unique and often much more complex. When new plats and replats are recorded, the subdivision covenants and declarations should be carefully reviewed by both administrative and appraisal staff before allocating values to the new parcels.

For the most part, allocations should be based on the same valuation unit, e.g., $ per acre, $ per square foot, etc., that was used to value the original parcel as of January 1 of the current year. Care must be taken to ensure that the total taxable value of the original parcel(s) equals the total taxable value of the new parcel(s). The value and classification established January 1 of the current year must not change until the following January 1.

In cases that are more complex, such as the replatting of mixed use properties, planned unit development parcels, condominium projects, or parcels with different zoning or agricultural soil types, these procedures may require more detailed allocation methods. In any case, it is necessary to maintain the classification and value of the original parcel as of January 1.

Splits and Mergers

- Review legal description in the transfer document.

- Locate the appropriate assessment map and plot the new legal on the map.

- Assign new parcel number(s) according to the map numbering sequence.

- Write an abbreviated legal description for metes and bounds descriptions.

- Determine acreage or square footage amounts, if necessary.

- Create new records as needed.

Return source document with new parcel number(s) to the transfer clerk.

Splits and mergers can be processed any time during the year. However, total parcel values are set as of the property status on the assessment date and cannot be increased or decreased for the year of the split or merger. Abstract codes should be assigned based on the use of the property on the assessment date.

Subdivision, Townhome, Condominium, and Pud Plats

- Obtain a copy of the plat.

- Appraisal file (all pages).

- Mapping file (first page only for condo plats).

- Review the plat, locate the appropriate assessment map, and plot the new legal on the map.

- Assign new parcel number(s) according to the map numbering sequence.

- Create new records as needed.

- Transmit a copy of the plat indicating the new parcel numbers to the person responsible for processing plats.

Boundary Changes for Taxing Entity

- Review the legal description in the source document.

- Locate the appropriate assessment map and plot the new boundary on the map.

- Assign new parcel number(s) according to the map numbering sequence if the boundary line splits an existing parcel.

- Update or create new records as needed.

- Return the source document to the person responsible for processing boundary changes.

Formation of a New Taxing Entity

- Accurately identify those parcels that lie within the boundaries of the new district. The legal description and map of the boundaries of the new district should be verified from the source documents.

- Once identified, the boundaries of the new district should be plotted onto the appropriate assessment maps and/or tax area maps.

- A list of the affected parcels based on the assessment or tax area maps should be verified with the assessor’s database. Where necessary, new tax areas should be created and mapped.

Map Maintenance

- Create new assessment maps as necessary when areas become densely platted.

- Manual or automated updates should be made to the assessment map mylars or computer generated maps on a regular basis and new paper copies printed as necessary.

Movable Equipment

All portable or movable equipment, which is not subject to specific ownership taxation such as dog racing gates and trash dumpsters, is valued and assessed as provided in § 39-1-103(5)(a), C.R.S. Also refer to §§ 42-3-102(1) and 103(3), C.R.S.

All owners of this type of property must file a Personal Property Declaration Schedule (Form DS 056). If the equipment is expected to be located in more than one county during the year, the owner indicates the counties and the estimated length of time it will be in each county. The assessor making the original assessment (county in which the equipment is first located during the current calendar year) apportions the value among counties affected according to the portion of the year, in days, the equipment will reside in each. A copy of the value is mailed to the equipment owner and to the assessor of each affected county. The value determined by the assessor of the county of original assessment is used by all county assessors involved, §§ 39-5-113(1) and (2), C.R.S.

However, if the equipment is moved into a county not included in the original apportionment, the assessor of the county requests an amended apportionment of value from the county originating the assessment. Failure to request an amended apportionment results in no assessed valuation for taxes on this equipment for the county not included in the original apportionment. If the amended apportionment of value is received by an assessor after the Abstract of Assessment has been filed, either an abatement or an additional assessment (omitted property) shall be made as necessary, § 39-5-113(3), C.R.S.

An exception is oil and gas rotary drilling rigs which are valued and assessed as provided in § 39-5-113.3, C.R.S.

Refer to Volume 3, Personal Property, Chapter 7 Special Issues.

Ports of Entry – Form 301

Mobile machinery and self-propelled construction equipment is generally registered with the county clerk for payment of annual specific ownership taxes in lieu of ad valorem taxation. Owners of equipment located in Colorado for only a portion of the year can also obtain a prorated registration through a Colorado port of entry. However, if such equipment is operated exclusively on property owned or leased by the owner of the equipment and never operated on a public road, the owner may declare it for ad valorem taxation. If such equipment must be moved through a port of entry, it may be detained without proof that the taxes were paid.

To avoid detention, the owner or agent may list the equipment on Form 301, and have it signed by the assessor or deputy in the county of original assessment. Refer to Volume 5, Personal Property, Chapter 7 Special Issues.

Omitted Property

Omitted property consists of any taxable property, such as personal property, land, an improvement, or both land and an improvement, that is not listed on the current assessment roll. A determination must be made as to how long the property has been omitted. Statutory provisions relating to omitted property are listed below.

- Omitted property is valued and assessed for the current year and up to two prior years when the error or omission is the fault of a governmental entity, § 39-10-101(2)(b)(II), C.R.S. If the omission is not the fault of a governmental entity, the omitted property can be valued and assessed for up to six prior years, unless fraud was committed with the intent to evade taxation, in which case there is no limit on how far back taxes can be collected, §§ 39-10-101(2)(b)(I) and (2)(c), C.R.S. However, omitted residential personal property cannot be assessed for a prior year when its discovery occurs as the result of an advertisement for the rental of the real property in which the furnishings are located, § 39-5-125(3), C.R.S. When property is valued for prior years in which it was omitted, the value must reflect the appropriate level of value for each such year. Oil and gas is the exception with omitted property provisions found in § 39-10-101(2)(d), C.R.S.

- Omitted property is added to the assessment roll as soon as the assessor discovers the omission. The assessor is also required to notify the treasurer of any unpaid taxes for prior years, § 39-5-125(1), C.R.S.

- Omissions and corrections on the assessment roll may be processed by the assessor at any time before the tax warrant is delivered to the treasurer, § 39-5-125(2), C.R.S.

- Once the tax warrant is delivered to the treasurer, the assessor notifies the treasurer of the omitted property and then the responsibility for omitted property, omissions, and corrections is assumed by the treasurer. Such actions are often referred to as “treasurer’s assessments,” §§ 39-5-125(2) and 39-10-101(2)(a), C.R.S.

- If the property is not omitted but there is an error in the name of the person owing taxes, the treasurer is to correct the name, and then collect the taxes from the proper party, § 39-10-101(3), C.R.S.

- The county board of equalization shall order the assessor to add to the assessment roll any omitted property which has come to its attention, § 39-8-102(1), C.R.S.

- All persons owning taxable personal property are required to make full and complete disclosure of their personal property for assessment purposes. If an owner does not make full and complete disclosure after two successive schedules have been mailed, or upon whom the assessor or his deputy has called and left one or more schedules, that owner’s taxable personal property is subject to a penalty of up to 25 percent of the assessed value of the omitted property. However, to apply the penalty, the following conditions must exist: 1) the assessor must allow ten days from the date of notification for the owner to make full and complete disclosure, and 2) the assessor must discover the property that was omitted (the Division recommends a physical inspection to discover property and a book audit to determine value), and 3) the owner must have previously filed a declaration schedule, listing his taxable personal property. This penalty also applies to any taxable personal property in a filed schedule which was represented by false, erroneous, or misleading information. For more information on this procedure, refer to ARL Volume 5, Personal Property Valuation Manual.

When adding omitted property valuation after the statutory close of the assessment period (CBOE can add after NOV deadline or assessor can add after CBOE hearings have concluded), care must be exercised to distinguish the difference between truly omitted property and an undervaluation. If the item of personal property, the improvement, or the land was not listed in the appraisal records and/or its value had not been placed on the assessment roll, the property has been omitted. If a value had been placed on the property and the taxpayer received a Notice of Valuation, and it is later discovered that the property has a greater value, the property has been undervalued and the value cannot be increased. Undervaluation does not qualify as omitted property, In Stitches, Inc., v. Denver County Board of County Commissioners, 62 P.3rd 1080 (Colo. App. 2002). The assessor should be prepared to defend omitted property additions to the assessment roll or tax warrant by use of records which substantiate the omission and the value attributable to the property.

Whenever it is discovered that any taxable property has been omitted from the assessment roll, the assessor shall determine the value of the omitted property and list the property on the assessment roll, as follows.

- Determine the number of years the property was omitted. The number of years for which a property can be assessed as omitted is discussed previously under this heading.

- Determine the classification (use) of the property.

- Calculate the value of the property for the current and any prior years it was omitted.

NOTE: The value must reflect the appropriate level of value the appropriate assessment rate Addendum 3-A, History of Data Gathering Periods and Assessment Rates details the correct level of value and assessment rates for past years. - Assign a parcel number or schedule number to the property, if necessary.

- Add the omitted property to the assessment roll.

Prepare and mail the owner a special notice of valuation (SNOV) and protest form for each year the omitted property is being assessed.

NOTE: You should provide 30 days for the owner to file an objection to the value with the assessor. Owners of real property may also protest the property classification. The assessor must make a decision on the protest and mail a special notice of determination to the owner within thirty days of the date the protest was filed.

If the assessor denies the protest, if the owner disagrees with the assessor’s determination, or if the owner does not receive a special notice of determination, the owner must file an abatement petition with the county after the tax bill is received in order to appeal the assessor’s decision. The abatement petition must be filed within two years of the January 1 following the year in which the taxes are levied. For omitted property, the taxes are levied on the date the tax bill is mailed. The abatement may be filed for any or all years the property was omitted. Refund interest for omitted property accrues from the date the completed abatement petition is filed or the date the taxes were received by the treasurer, whichever is later.

- Notify the treasurer of the taxes due for prior years.

NOTE: The tax calculation must reflect the appropriate mill levy and assessment rates for the omitted tax years. A history of assessment rates is found in Addendum 3-A, History of Data Gathering Periods and Assessment Rates of this chapter.

Omitted Revenue

When taxable property is assigned to the wrong tax area, or when the boundaries of a tax area are drawn incorrectly, some properties listed on the tax warrant may not include the mill levy for one or more taxing entities. Such an event is similar to omitted property in that the properties and their owners may benefit from the services provided by the taxing entity without being subject to the entity’s mill levy. This may result in a loss of revenue to the taxing entity and/or a greater tax burden imposed upon other taxpayers.

When such an omission is caused by assessor error, such as failure to process a recorded inclusion order, the question arises as to whether a correction should be made for prior years or only for the current year forward. Section 39-10-101(2)(a)(I), C.R.S., allows the treasurer to assess and collect taxes for property that was omitted from the tax warrant and not valued for assessment. If the situation above is interpreted literally, the properties in question do not satisfy these requirements.

However, in Aggers, Assessor, v. People Ex Rel. The Town of Montclair, 20 Colo. 348, 38 P. 386 (1894), the court reviewed the occurrence of such an omission and determined that omitted revenue should be collected. In this case, the assessor had failed to extend the mill levies certified over multiple years by the Town of Montclair to property that had been annexed to the town. The town argued that it was entitled to the collection of omitted revenue pursuant to the predecessor statutes to §§ 39-10-101(2)(a)(I) and 39-5-125, C.R.S. The court agreed, finding that although the situation did not fall within the strict letter of statute, it was clearly within its spirit and intent.

The purpose of the statute evidently is to prevent property from escaping taxation through oversight, omission or mistake, and to enable the taxing officers to impose upon all property its just and equal proportion of the public burden. The strict construction contended for by counsel for respondent would prevent the accomplishment of this object and purpose . . . .

No reason can be perceived why the omission to extend or enter the taxes upon property listed and valued would justify the exemption of such property from taxation, when the omission of the property itself from the tax list would not do so (20 Colo., page 351).

The basis for the Aggers decision remains valid today. From the perspectives of the affected parties, namely, the property owner(s), the taxing entity, and the other taxpayers serviced by the taxing entity, when a tax area is assigned incorrectly, the error can result in the non-extension of an entity’s mill levy. The error has the same effect on the parties, as would the omission of the property itself from the tax warrant. Therefore, if the omission was an assessor error, the property is subject to the collection of up to two years’ omitted revenue. A Special Notice of Valuation is not mailed because no change is being made to the value or classification of the property. However, a letter of explanation should be sent to the taxpayer.

If the Board of Assessment Appeals, District Court or an arbitrator orders an increase in value, the assessor makes the correction to the year(s) ordered and presents the order or judgment to the county treasurer who subsequently processes the difference as omitted property according to § 39-10-101(2)(a)(1), C.R.S.

The reporting of omitted revenue to taxing entities on their certification of values is discussed in Chapter 7, Abstract, Certification, and Tax Warrant under 5.5 Percent Statutory Property Tax Revenue Limitation.

Out-of-State Ownership List

The assessor shall furnish annually, by the first day of June to the Department of Revenue a list of the names and addresses of all nonresidents of Colorado who own real and personal property in the county as shown in the assessors records as of the previous assessment date, § 39-5-102(3), C.R.S.

Although the law only requires the name and address of the nonresident, the Department of Revenue requests counties to provide the additional information shown below, using a Microsoft Excel format:

| Column Name | Column Format | Max. Column Length (# of Characters) | Additional Guidelines |

|---|---|---|---|

| County | Text | 35 | The County should be spelled out (i.e., Denver, Weld) |

| Parcel | Text | 35 | |

| SubClass | Text | 20 | |

| Owner Name1 | Text | 100 | |

| Owner Name 2 | Text | 100 | |

| Owner Address1 | Text | 100 | The Address fields should be in one column (W 123 S Main Blvd) , not broken up into separate columns (W), (123), (S),(Main),(Blvd) |

| Owner Address 2 | Text | The Address fields should be in one column (W 123 S Main Blvd) , not broken up into separate columns (W), (123), (S),(Main),(Blvd) | |

| Owner City | Text | 50 | |

| Owner State | Text | 2 | |

| Owner Zip | Text | 9 | |

| Physical Address | Text | 50 | The Address fields should be in one column (W 123 S Main Blvd) , not broken up into separate columns (W), (123), (S),(Main),(Blvd) |

| Location City | Text | 50 | |

| Actual Value | Currency | 99,999,999,999.00 | The Actual Value field doesn’t have an actual set length, but the field should be a Currency format with two (2) decimals. |

The data may be e-mailed, or a CD or disk may be mailed to the address below.

Department of Revenue

Audit Selection Committee

Attn: Mr. Lauren Hagge

720 South Colorado Boulevard, North Tower, Suite 400N

Denver, CO 80246

Phone: 303-692-7938

Email: lauren.hagge@state.co.us

Questions concerning electronic submissions should be directed to the Audit Selection Committee at the above telephone number.

Personal Property Issues

After the Assessment Date

If a firm commences business after the assessment date, the property is taxable January 1 of the year following the year it is put into use, § 39-5-110(1), C.R.S. When personal property is newly acquired and put into use, it becomes taxable the following January 1 if the property is used for business purposes, § 39-3-118.5, C.R.S. If the property is in storage, it does not become taxable until January 1 following the year it is put into use, §§ 39-5-104.5 and 110, C.R.S. Refer to ARL Volume 5, Personal Property Valuation Manual, for further information.

The personal property of a firm that quits business after the assessment date is taxable for the entire year, § 39-5-104.5, C.R.S. If either the assessor or treasurer believes that personal property may be removed, dissipated, or distributed so that taxes may not be collected, the treasurer may proceed to collect the taxes immediately, and, if necessary, distrain, seize, and sell the personal property, §§ 39-10-111(1)(a), and 113(1)(a) and (2), C.R.S.

Incentive Payments

A county, municipality, or special district can enter into negotiations for an incentive payment with owners of new business facilities. A county, municipality, or special district may also negotiate an incentive payment or credit with owners of existing business facilities, located in their jurisdiction, based on verifiable documentation demonstrating that there is a substantial risk that the owner of the existing business facility will relocate it out of state. The incentives cannot exceed 100 percent of the personal property taxes paid to the county, municipality, or special district. For agreements made prior to August 6, 2014, the agreement cannot last more than ten years. For agreements made after August 6, 2014, the agreement may not last longer than thirty-five years, §§ 30-11-123, 31-15-903, and 32-1-1702, C.R.S. Additional incentives are available through income tax credits, real property tax incentives, and sales tax refunds. For further information on these incentives refer to §§ 39-30-105.1 and 107.5, C.R.S.

Personal Property Moved in or Out of State After January 1

Personal property is valued as of the assessment date and is valued for the entire year regardless of any destruction, conveyance, relocation, or change in taxable status, § 39-5-104.5, C.R.S. Personal property removed during the assessment year is taxable for the entire year, § 39-5-104.5, C.R.S. The owner of any personal property that is removed from the state is liable for the entire tax obligation, § 39-5-110(2), C.R.S. When taxable personal property is brought into the state after the assessment date, the owner must complete and file with the assessor a personal property declaration schedule if the actual value of the personal property exceeds the exemption threshold shown below, § 39-5-110, C.R.S.

Personal property is exempt if its actual value is equal to or less than the exemption threshold shown for the applicable tax year. Exempt personal property accounts should be flagged and reviewed annually.

| Tax Year | Exemption Threshold |

|---|---|

| 2009 – 2010 | $4,000 |

| 2011 – 2012 | $5,500 |

| 2013 – 2014 | $7,000 |

| 2015 – 2016 | $7,300 |

| 2017 – 2018 | $7,400 |

| 2019 – 2020 | $7,700 |

| 2021 – 2022 | $50,000 |

| 2023 - 2024 | $52,000 |

| 2025 - 2026 | $56,000 |

| Thereafter | Inflation factor calculated by the Division |

Exemption of Consumable Personal Property

In 2000, the general assembly amended § 39-3-119, C.R.S., to require the Division of Property Taxation to “publish in the manuals, appraisal procedures, and instructions prepared and published pursuant to § 39-2-109(1)(e), a definition or description of the types of personal property that are ‘held for consumption by any business’ and therefore exempt from the levy and collection of property tax pursuant to this section."

The Division has developed two criteria to aid in determining whether personal property is considered consumable, and therefore, exempt from property taxation. To be classified as “consumable,” personal property must fall under one of the two criteria identified below:

The personal property must have an economic life of one (1) year or less.

This criterion applies to any personal property regardless of original acquisition cost. This category also includes non-functional personal property that is used as a source of parts for the repair of operational machinery and equipment.

The personal property has an economic life exceeding one year, but has an acquisition cost, inclusive of installation cost, sales tax, and freight expense to the point of use, of $350 or less.

The $350 personal property threshold applies to the acquisition cost of the personal property as completely assembled for use in the business, not the personal property’s unassembled, individual component parts.

For leased equipment having a “buyout” provision occurring during or at the end of a lease, the fair market value of the personal property, including installation, sales tax, and freight to the point of use, at the time the initial agreement is executed, is to be used as the acquisition cost for the purposes of the $350 threshold.

Processing Declarations

- Date stamp declaration schedule.

- Verify that the declaration schedule was timely filed.

NOTE: If the schedule is filed after the deadline, it is necessary to staple the envelope showing the postmark to the declaration schedule. - Match declaration schedule with personal property file.

- Review for address and/or ownership changes and for owner’s social security number or federal identification number.

- Review the Personal Property Declaration Schedule. Determine if the form was properly completed and signed by the property owner or agent. The itemized list of personal property may be shown on the declaration schedule or furnished on an exhibit attached to the declaration schedule, § 39-5-108, C.R.S.

- Review the file for audit notes or other documentation that should be referenced during processing.

- Review the current personal property record and make necessary adjustments. Review and reconcile the asset listing and/or depreciation schedule. Check for other assets that may not be listed in the addition and deletion portion of the declaration schedule.

- Check for leased equipment reported on the declaration schedule. This tracking can be done manually or electronically.

- Enter property changes into the computer system.

- File personal property record.

Physical Inspection of Real Property – Guidelines

A notice should be placed in a local newspaper stating that the assessor’s office is conducting property inspections in specified neighborhoods. The notice should also indicate that the appraiser will leave an informational door hanger to schedule an appointment if no one is home. Each assessor’s office should develop a property inspection form to assist appraisers as a check list for conducting efficient, thorough and uniform inspections.

Prior to Field Inspection

- Contact the property owner and establish a time to inspect the property.

- Pull and review the appraisal records and all the pertinent information (building permits, TD-1000, sales verification letters, agricultural classification questionnaires, etc.) that pertains to the property.

- If the location of the property is unknown, obtain and reference an assessment map to identify the property location.

- Make sure the following items are available and in working order:

- Camera and memory card

- Measuring tape

- Flashlight

- Calculator

- Protective wear (boots/old shoes, rain gear, etc.)

- County identification

- Paper and pencil

- Property inspection forms.

- Pertinent subject properties’ appraisal records

Field Inspection