General Objectives

The duties of the assessor, as expressed in the Colorado constitution and statutes, can be summarized into four categories: the discovery, listing, classification, and valuation of taxable property. The four categories are sometimes referred to as the assessment function. Most taxable property is subject to biennial valuation, while certain categories of property, such as personal property and natural resource, producing mines, and oil and gas leaseholds and lands, are valued each year. To accomplish these tasks, the assessor must plan for and implement an assessment program. The guidelines found in this chapter to assist Colorado assessors in researching and identifying their individual needs and to translate those needs into a detailed written plan.

Specific County Objectives

Planning involves setting objectives and then developing strategies through which the objectives can be accomplished. The objectives of an effective assessment plan are:

- To establish guidelines for an adequate budget, competent staff, and internal controls.

- To establish specific assessment practices that achieves uniformity and consistency through fair, equitable, and defensible values.

- To establish mechanisms to complete the assessment function.

Essential Planning Guidelines

The following planning guidelines are offered to aid the assessor in the planning process:

- Establish general goals and specific objectives with key personnel for an annual assessment plan for personal property and a biennial assessment plan for real property.

- Evaluate existing practices and processes to determine the merits and deficiencies that exist.

Establish procedures to meet goals and objectives through a comprehensive written plan including both real and personal property. The plan should include what needs to be done, who needs to do it, what resources are available or needed, and the reasonable timeframes required to complete each task.

Additionally, a personal property audit plan is mandated by the State Board of Equalization. The following topics should be included in the county audit plan:

- Purpose of the plan; personal property account characteristics;

- Plan timeframe and interim progress review points;

- Listing of office resources involved in the audit program;

- Account review selection criteria and specific audit “triggers”;

- Audit work paper and documentation guidelines; and

- Assessor signature page.

The plan must be reviewed each year and updated as needed. Recommendations for specific information to be included under each of these topics can be found in ARL Volume 5, PERSONAL PROPERTY VALUATION MANUAL, Addendum 5-A, Audit Standards.

- Determine workload areas; workforce requirements; equipment needs to complete the annual assessment plan; and the cost to accomplish these tasks.

- Present the annual assessment plan and budget requirements at the assessor’s scheduled budget meeting with the board of county commissioners. The assessor should clearly identify the duties mandated by the constitution, statute, and the State Board of Equalization, and explain the ramifications of non-compliance.

- After approval, review the plan with staff and start implementation. If the budget request is not fully approved, first review and modify the plan to fit the approved budget and to complete the statutorily required duties of the office before presentation to the staff and implementation.

- Establish procedures for evaluation of the results.

- Establish components for a public relations program.

Assessment Practices

Mapping

The administration of a successful real property appraisal is dependent on proper mapping of the county. The appraisal personnel will need adequate maps at a scale large enough for the identification of individual parcels, subdivisions, blocks, lots, and streets. The mapping system may be a simple drafting system or a sophisticated computerized geographic information system (GIS). Ideally, the county should also be completely parceled in accordance with approved mapping specifications. For additional information concerning mapping specifications and parcel guidelines, refer to Chapter 14, Assessment Mapping and Parcel Identification.

Assessment maps are essential for the following general uses:

- Master control: An overall county map should be used to show progress and time projections for the completion of the biennial reappraisal.

- Appraisal staff: Work maps for the appraisal staff should be available. Use of these maps is detailed later in this section.

- Tax entity and tax area maps: These maps ensure that each property is listed within the proper taxing entities and tax area.

Geographic Information System

The geographic information system stores maps as computer databases. Various kinds of information are often stored in different layers. The databases can be combined and analyzed in many different ways to produce maps for specific needs in a variety of forms. The base map generally has the parcel boundaries and parcel identification numbers. One layer may contain property characteristics such as streets, rivers, and highways. A second layer may show the various tax areas, a third layer may show zoning information, while a fourth layer may contain topographical or aerial features, and so on. A great variety of spatial analysis can be performed through the overlaying or merging of different data layers. Many counties use GIS as an appraisal tool by linking their computer-assisted mass appraisal (CAMA) data to the various layers. Sales maps can be created showing the location and sale price of sold properties and the assessor’s values for each property. Comparable amenities may also be analyzed, such as building square feet, land size, price per square foot, and other relevant data.

Creating a GIS is usually a cooperative effort among several county offices. The base map containing parcel information is essential to the system.

Specifications and guidelines for computer-assisted mapping can be found in Addendum 14-A, Guidelines for Assessor Digital Parcel Mapping.

Land Sales Map

The real property appraisal program begins with the valuation of the land. The most valid and supportive method of land valuation is through the sales comparison approach. However, except for improved residential land, all other methods to determine land value must be considered in accordance with § 39-1-103(5)(a), C.R.S. Sales maps are a vital tool in the completion of a proper revaluation.

For a detailed description of land valuation methods, refer to ARL Volume 3, REAL PROPERTY VALUATION MANUAL, Chapter 2, Appraisal Process, Economic Areas, and the Approaches to Value, and Chapter 4, Valuation of Vacant Land Present Worth.

Information that can be shown on sales maps by parcel includes:

- Sale date(s)

- Confirmed sale price of all sales occurring during the time period prescribed by statute.

- Confirmed sale price converted to a price per comparable unit

- Land size and dimension

- Classification code (refer to Chapter 6, Property Classification Guidelines and Assessment Percentages)

- Analysis of comparability (neighborhood boundaries, physical differences in topography, etc.)

- Assigned actual value

- Zoning which can determine legal land use

- Neighborhood and economic area boundaries

In addition to the maps, the above information should be entered in a computerized database for analysis. If the county is not using a computer-assisted mass appraisal system that is capable of statistical analysis, this information can be entered into a commercially available database or spreadsheet program. All atypical characteristics of a property should be noted.

The statistical analysis should minimally include calculating measures of central tendency for sales ratios (mean, median, and weighted mean); measure of uniformity (coefficient of dispersion); and a measure of assessment bias (price-related differential) for various strata of sales (by property class, economic area, neighborhood, architectural style, size, age, etc.). A more thorough analysis will include tests for validity, reliability, and sampling size. Additional information concerning statistical analysis can be found in ARL Volume 3, REAL PROPERTY VALUATION MANUAL, Chapter 8, Statistical Measurements.

Improvement Sales Maps

Maps for residential, commercial, and industrial properties should be kept current and show the following items when possible:

- Improved parcels

- Type of improvements

- Sale date(s)

- Confirmed sale price occurring during the time period prescribed by statute

- Classification code

- Assigned actual value

- Zoning which can determine legal land use

- Neighborhood and economic area boundaries

Information for qualified/verified sales, along with income and expense data, should be entered into the database for analysis of commercial/industrial property. Also, number of units, number of stories, value per unit, and atypical property characteristics can be analyzed at this time.

Real Property Ownership Files

The assessment roll database is the primary real property ownership file. It should be based on the parcel identification number. Minimally, it should contain: the name of the owner, the owner’s mailing address, legal description of the property (often abbreviated), current actual and assessed valuation, tax area code, and classification code. The file should be cross-indexed by owner’s name, property address, and parcel identification number.

Real Property Characteristics File

The real property characteristics file, or property record, contains data for each property. It documents the factors and methods used in appraising each property. The file records are examined and revised regularly.

Typically the file includes the parcel identification number, street address, site characteristics, improvement characteristics, building(s) perimeter sketch, building permit history, sales history, record of inspections, the cost, market and income approaches to appraisal data, photograph(s) of the property, newspaper articles, correspondence (unless confidential), and assessment appeal history. Thus, the property characteristics file is essentially a record of the current status of properties and in some cases may provide a five to ten year assessment history.

Many counties not only have easily accessed electronic files for this data, they also have websites wherein most of this information is readily available to the public through the internet.

Real Property Sales File

The sales file is a record of all documentary fee and non-documentary fee transfers of real properties recorded with the clerk and recorder. This should be an ongoing list that can be accessed for analysis. The sales file should contain:

- Parcel or identification number

- Physical description of the sold property as of the date of sale

- Confirmed sale price

- Actual value

- Book and page or reception number of conveyance document

- Address or legal description of the property

- Use and zoning codes

- Sales disqualification code (if applicable)

- Source of verification (TD-1000, MHTD, letter, telephone, in-person, buyer, seller, agent)

- Neighborhood and economic area code.

The file is distinct and independent from the property characteristics file because it only contains information on properties that sold or transferred. Qualified sales that were sold within the data gathering period will be used to establish appraisal models and defend the values set by the appraisers. Additional information concerning sales files and confirmation of sales can be found in ARL Volume 3, REAL PROPERTY VALUATION MANUAL, Chapter 3, Sales Confirmation and Stratification.

Real Property and Sales Data

Real Property Classification

Proper classification coding will provide essential property information for many governmental organizations to use for planning, legislative impact studies, and statistical measurement. For the assessor, correct coding is essential to establish equitable values, proper assessment percentages, and to determine growth patterns of neighborhoods and economic areas. For more information concerning classification descriptions, refer to Chapter 6, Property Classification Guidelines and Assessment Percentages.

Physical Characteristics Collection

Appraised values are only as accurate as the property data upon which they are based. Of primary importance is data related to the physical characteristics of each property. Current, accurate physical data will ensure effective application of the cost, market, and income approaches to value. The collection of current physical characteristics data can be obtained through the implementation of complete physical appraisal and drive-by review programs, which are systematically scheduled. Also, if the county and municipalities have building inspection departments, the assessor should acquire copies of the issued building permits on a regular basis.

Sales Confirmation Program

An ongoing and well organized sales confirmation program is the most vital element in the collection of accurate sales data for the general appraisal of real property. Sales confirmation, which involves the discovery, collection, listing and confirmation of sales, is essential to the effective application of the three approaches to value and the development of a reliable assessment ratio analysis program. A good sales confirmation program involves both administrative and appraisal personnel, and it must be continuously administered because properties sell or transfer throughout the year. For additional details on the sales confirmation process, refer to ARL Volume 3, REAL PROPERTY VALUATION MANUAL, Chapter 3, Sales Confirmation and Stratification.

Data Processing and Record Storage

Computers are used for many administrative functions such as printing and storage of property data, generating notices of valuation, compiling reports for the Abstract of Assessment, and producing the tax warrant. Many other reports may be produced, such as:

- New and deactivated parcel lists

- Value change audit reports

- Edit reports with error and warning messages

- Cross reference indexes

- Building permit listings

- Classification code listings

- Property neighborhood and economic area listings

- Provide data which support the annual budget.

- New construction lists which are used in calculating both the local growth factor and the 5.5 percent statutory property tax revenue limitation.

Other local agencies, such as a county or municipality planning department and a downtown development authority, may also use computerized information in the assessor’s database.

Computer technology lends itself to appraisal applications. The major advantage of computer-assisted mass appraisal systems is improvement of assessment uniformity and quality. Some of the most common appraisal applications are:

- Cost approach

- Market approach

- Income approach

- Reconciliation (Correlation)

- Statistical reports for specific factors:

- Economic area and neighborhood analysis

- Time trend analysis

- Market adjustments

- Property use

- Resold properties

- Sales-ratio studies

- Market depreciation studies

- Simple linear and multiple regression analyses

The internet, in combination with a real property database and GIS, has greatly expanded the assessor’s ability to make public records accessible to the general public. Many counties have a website that contains much, if not all of the information in their public databases, as well as parcel maps and sales lists.

Personal Property Data

Personal Property Appraisal

Unlike real property, which is predominately subject to a biennial cycle of review and value determination, personal property is reviewed each year in accordance with the assessor’s mandated personal property audit plan and valued annually utilizing reported data. One of the most difficult jobs for a county assessor is the discovery of personal property. However, good discovery practices will yield positive results in accurate property records and assessments. Personal property discovery must be an ongoing task because personal property is movable and may leave the county faster than the assessor can discover it. A thorough program of discovery must be created and maintained to ensure accurate property listings. Inaccurate property listings mean that certain personal property owners may escape paying their legal share of property taxes.

In addition to locally assessed personal property, most of the value of state assessed companies is classified as personal property. The state assessed companies are valued by the Division of Property Taxation. The Division is responsible for responding to protests and appeals of value. Determining and defending the state assessed values by the Division removes much of the workload away from the assessor. For more information concerning state assessed property, see Chapter 11, State Assessed Property.

Personal Property Ownership Files

The personal property listing process begins by setting up account records for owners of taxable personal property. A cross-check should be conducted on existing office records to determine if a new business is filing under another name and/or at another location. An assessor’s staff member should call or visit the property owner to gather any necessary information for the listing process. A primary source of personal property discovery is the annual declaration schedule. After the names of the businesses and owners have been recorded in the personal property account records, a declaration schedule is mailed. It is especially important that owners of personal property located in the county on the January 1 assessment date receive the declaration schedule as soon after January 1 as possible. Additional details regarding the personal property declaration schedule can be found in ARL Volume 5, PERSONAL PROPERTY VALUATION MANUAL, Chapter 2, Discovery, Listing, and Classification.

Accurate property appraisal files must be maintained for each personal property owner. These files, and their associated records, serve as the permanent documentation for any assessments made by the assessor. The files are the repository of all information gathered by the assessor regarding the owner’s property. Files should include all declaration schedules and documents submitted by an individual owner or business, along with appraisal records, worksheets, copies of notices of valuation, correspondence, and any other data pertaining to that specific owner or business. These records contain confidential information, such as detailed lists of personal property reported by the owner. There are statutory penalties for divulging confidential information.

To provide overall control of the ownership files and records, a permanent unique personal property account identification number should be assigned to each account. Account identification numbers provide for control accounts. They also enable the assessor to keep records for similar types of businesses together for easy reference and comparison, on a business-by-business basis, when needed.

Public Relations

Every assessor’s office should have an effective public relations program that conveys what the office does, and how, why, and for whom its services are performed. An effective public relations program in the assessor’s office provides current and useful information regarding the laws, policies, and operations affecting the assessment of real property. It can result in more accurate and thorough coverage from the news media, a better informed public, and an increased awareness of the important role that property tax plays in the funding of local government. Public outreach prior to sending the biennial revaluation notices of value can greatly assist in lowering protest numbers.

An integral part of the public relations program is quality customer service. In many ways, it is the front line in the assessor’s efforts to improve his or her image with the public. Daily contacts between the assessor’s office and the public via the telephone, questions at the counter, and contact in the field set the tone for the public’s impression of the office. “Customer service is an attitude. It can be expressed in terms such as thoughtfulness, courtesy, integrity, reliability, helpfulness, and efficiency” (Tschohl 1991).

Effective public relations can be categorized into three phases:

- Determine the public relations needs

- Develop a comprehensive public relations plan

- Implement the plan

Phase one consists of observing public opinion and determining what the concerns are. Is the new assessment level a major issue? Why are the assessor’s appraisers physically reviewing all properties on the north end of town? Is the public aware of the role of the State Board of Equalization? What was the latest legislation passed concerning property valuations? The assessor and key personnel should establish a plan to address any areas that may have a negative impact on the office. By anticipating problems, strategies can be developed for addressing them in advance. Part of this anticipation should be the development of an office response that all staff can relay to the public. A uniform message from the staff conveys to the public that the assessor’s office is informed. Staff will also be more confident dealing with the public when the public’s response has been anticipated. All staff should be well versed on the most frequently asked questions and the appropriate office responses.

Phase two is developing an effective plan to answer the questions and concerns observed in phase one. The public relations plan should include:

- The timing of each public relations event

- Justification of the selection of the media used

- An outline of the contents or subject matter of each event

- A list of relevant guidelines to be used in explaining the situation to property owners

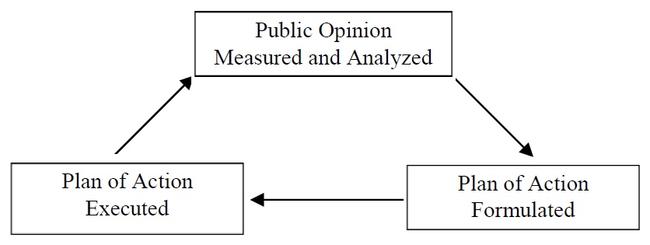

Phase three is execution of the plan developed in phase two. Public opinion has been recorded and analyzed, objectives have been formulated, and a plan constructed. Now the plan must be carried out.

Each of these phases operates simultaneously, since public opinion can change constantly. For this reason, the public relations plan must be flexible with actions corresponding to the needs of both the property owner and the assessor. The following diagram illustrates the continual process of the three phases of public relations:

The assessor is highly dependent on other parties to fulfill their job requirements. Some of these other parties are:

- Board of county commissioners for budget appropriations

- Other county and governmental agencies for such data as zoning, building permits, building regulations, and recorded documents

- Software vendors for accurate reliable software to assist in the valuation and reporting of mass appraisal values

- Banks, real estate agencies, appraisers, developers, and title companies for sales data, sales confirmations, sales trends, and correct title chains

- Property owners for sales, income, and expense data

The assessor can encourage the above participants by conducting an effective public relations program.

Staffing

In order for the assessor to discover, list, classify, and value all property in the county, adequate staff and organization plans are needed. The number of staff in an assessor’s office is influenced by many factors. Some of these factors are: size of county, rate of growth in new construction, complexity and capabilities of appraisal program and mapping software, and non-assessment duties of the assessor.

Production Planning

“Production planning” is a term borrowed from the manufacturing sector that refers to the creation of a plan or chart to explain the interaction of various work stations in the production process. Production planning of assessment activities can lead to a more accurate estimation of the time estimates for each task and may result in a more efficient use of office personnel and resources. Annual calendars showing appraisal and administrative production quotas by month are some examples of production planning. Meeting or exceeding the established quotas will assure that all activities are completed within a planned time and that statutory deadlines are met. If the quotas are not consistently met, an additional study should be conducted or processes should be reviewed to determine the problem. The problem may be that the quotas are unreasonable for the time necessary to perform specific activities; the staff is not managing its time well, the overall process is cumbersome and needs to be “streamlined,” or a combination of these reasons. If production consistently exceeds the quota, activity planning and the appropriate quota should be reanalyzed and revised as well.

Internal Controls

A set of internal controls is essential to the effective and efficient functioning of an assessment system. Internal controls ensure that laws, policies, and regulations are followed, standards of appraisal accuracy are maintained, work is finished on time, and resources are used efficiently. The degree to which internal controls should be formally set depends upon the size of the assessor’s staff. A larger staff requires more extensive controls. The five major types of internal controls are:

- Office organization

- General workflow plan

- Standards of practice

- Monitoring procedures

- Record security procedures

Office Organization

The primary objective of an office organization plan is to allocate duties to appropriate personnel and avoid duplication. An office organization plan consists of two parts:

- Office organization chart

- Statements of function and responsibility for each employee

The office organization chart is a graphic representation of supervisory positions and lines of authority for all employees. The chart should be prepared so that the chain of command is clear to everyone. It should show the hierarchy of reporting relationships of departments and personnel and the number of people assigned to each function.

The basic office organization chart can be divided into three distinct groups. These groups are:

- Management Team

- Administration Team

- Appraisal Team

Each team, while being an integral part of the whole, has an important specialized function of its own. The Administration Team requires technical expertise in the administrative, mapping, listing, and reporting functions of the assessor. The Appraisal Team requires a staff of technically trained and licensed appraisers to value property. The Management Team may consist of the assessor, administrative officer (chief deputy), and the chief appraiser. The Management Team must coordinate the efforts of all teams, as well as perform the management function. Depending upon the staffing size of an office, additional divisions may occur within each team. For example, the Appraisal Team may have a further division into a Real Property group and a Personal Property group. The Real Property group may also be further subdivided into the various types of property being appraised, such as Land, Residential, Commercial, and so on.

Along with an office organization chart, statements of team functions and personnel duties and responsibilities should be outlined in writing. This will give each employee and Management Team member an understanding of the nature of the work and the level of performance expected. This is customarily done using a generic county job description form which has open areas to fill in the individual job description or a specific job description form developed within the assessor’s office.

Once an office organization chart has been drafted, the assessor must determine if the workforce needs are being met. Projecting adequate workforce for the assessor’s office on an annual basis requires analysis of the time requirements of both administrative and appraisal activities within the office.

General Workflow Plan

The general workflow plan should show the functional organization of the office. The physical arrangement of the office should be planned to enhance the internal controls that have been established and to maximize the efficiency and comfort with which employees perform their job duties.

Standards of Practice

An efficient assessment system requires that each function or procedure be performed in a complete and professional manner. Quality assurance procedures are a key to maintaining the soundness and integrity of any valuation system. This is important for single or repetitive functions such as processing property transfers or measuring and diagramming a building. Written standards of practice should be prepared for personal conduct, property characteristic observation and description, data processing codes, and completing office and inter-departmental forms.

Monitoring Procedures

The assessment system cannot operate effectively without some form of monitoring or “quality control” procedures. These procedures check for progress and performance of office functions and personnel. Some typical monitoring procedures include:

Time and Production Reports

Having employees keep records of the time they spend on various activities not only serves as a gauge for individual performance, but also assists in time management, scheduling, budget planning, and workforce requirements studies.

Sales Ratio Studies

This is the primary method of evaluating appraisal performance. The assessor should have appraisal analyses programs in place to test performance. Statistical analyses of the sales ratio data are ongoing indicators of appraisal performance. For additional information on statistical measurements, refer to ARL Volume 3, REAL PROPERTY VALUATION MANUAL, Chapter 8, Statistical Measures.

Data and Procedural Audits

While sales ratio studies evaluate overall appraisal performance, the administrative functions within the assessor’s office also need to be monitored. Automated and manual computer data entry and procedural audits monitor both the completeness and accuracy of data. An active on-going monitoring system should be in place to edit daily work. Internal edits are particularly important in fully automated systems to ensure that errors do not become universally applied. Because of the nature of the assessor’s work, the administrative and appraisal data files are constantly being updated. Some of this updating concerns ownership, mailing addresses, legal descriptions, and other changes to “literal” information. While input errors to these data entry fields can be serious and should be subject to a review process, they do not affect the valuation of a parcel. However, other input errors, such as value prorations, abstract coding, split or merged assessments, square footage measurements or other property characteristics, and neighborhood coding have the potential of producing significant assessment valuation errors. If such errors are not discovered before critical reporting and processing, such as in the notices of valuation, the distribution of state assessed values, the Abstract of Assessment, and the Certification of values to taxing entities, required corrections can be publicly embarrassing. When errors are discovered after the publication of the tax warrant, remedies are limited and costly. The errors also create public relations problems. Therefore control total audits can assist in reducing this possibility.

Control Total Audits

A two-phase control audit procedure should be implemented: Phase one is designed to detect such general input errors, and phase two is designed to correct the property record for the parcel where the error occurred. The actual procedure may vary according to the reporting capabilities of the computer system. Additional guidelines on control can be found in Chapter 7, Abstract, Certification, and Tax Warrant. However, every procedure should incorporate the following elements:

Phase one is a summary report or series of reports run on the entire database file with the same acceptable value ranges for classes and subclasses of property at regular intervals. Exception reports listing properties outside these value ranges are analyzed. For example, a summary report of all residences that have an appraised value over $500,000 can be generated. Comparing this report with the previously run report can spot properties inadvertently overvalued due to an entry error.

Class and subclass totals can be compared to corresponding totals on subsequent report(s). One report most counties run is the in-house abstract report for this audit. Unexplainable significant differences should then be researched. Typically, phase one reports are totaled by class and subclass of property, but may also be totaled by tax area or taxing entity.

A summary report of the state assessed values from the database should be compared to the notice of value provided by the Division of Property Taxation. The database values should exactly match the values on the Division’s report.

A summary report delineated by abstract code and value for each abstract code can indicate errors of improper coding between the land and improvements.

In phase two, corrections are made and the phase one reports are rerun to ensure the errors have not been compounded. Some assessors use the notice of valuation preview report for phase two because it will show differences between the prior year’s assessment and the current year’s assessment on a parcel-by-parcel basis.

The frequency of audits may depend upon the activity in the county, but the Division recommends that the abstract report should be produced and reviewed on a monthly basis. Some counties may run audit reports daily or weekly. If control total audits are performed on a regular basis, valuation, classification, tax area, etc. errors are discovered within the office and can be corrected prior to the completion of critical reports. For additional discussion, refer to pages 1 and 2 of Chapter 7, Abstract, Certification, and Tax Warrant.

Supervisory Review of Appraisals

Supervisory review is another means of evaluating accuracy and uniformity of appraisals. Difficult or complex appraisal assignments and appraisals completed by new appraisers should always be reviewed. It is also advisable to review a random sampling of all appraisals completed by the appraisal staff to ensure that good appraisal judgment is applied consistently and similar properties are treated similarly by different appraisers.

Record Security Procedures

The integrity of the assessment system cannot be maintained without some form of record security procedures. Such procedures could be in the form of record modification restrictions and/or authorization and “audit trails” of daily changes made to property records. The public should be limited to “read only” access to the database files on in-house computers. Website data is normally a periodic copy of “live” data with no ability for modification by the user. Great care must also be taken to preserve those records which are confidential and not available for public viewing, such as the reported information on the Real Property Transfer Declaration, the Manufactured Home Transfer Declaration, and all of the personal property and natural resource schedules and forms. Additional confidential data sources include: commercial property income data; veteran with a disability tax exemption applications; and senior property tax exemption applications.

Office Performance Evaluation

With the myriad of changes that may directly affect the overall performance of the assessor’s office, it is necessary to periodically review the internal controls. These changes can result from legislation, new policies, and advances in technology. For example, the legislation affecting titled manufactured homes in which their valuation and assessment transferred from the county clerk’s office to the assessor’s office required a major adjustment in the assessor’s office. Internal controls are best reviewed in an intervening year between revaluations. Occurrences such as budget cuts, a loss of trained staff, or a computer software conversion may require an immediate review. The depth necessary for the review is dependent upon the number and degree of changes that have occurred since the last review. The review should answer such questions as:

- Does the overall flow of work in the office system progress in an orderly manner?

- Can any segment of this flow be streamlined to eliminate redundancies and make the office system more efficient while maintaining the needed integrity?

- Are the individual task assignments within the office system adequately staffed?

Management can also discover many of the inefficiencies within the current office system during the periodic employee performance evaluations. Feedback from the individual employees can point out office system problems that may have been overlooked by management.

Budget Requirements

The most important part of an effective assessment system is an adequate budget. Recognizing the statutory duties of the office, a budget should be economical but sufficient to maintain an accurate database, personnel, and support services for the coming fiscal year.

Each year, the assessor prepares a budget, which is presented to the board of county commissioners. The assessor should prepare a detailed budget, which explains why each expense item is being requested with documentation and constitutional or statutory cites for all duties that are required to be completed by the assessor. Generally, being well-prepared to present the budget to the commissioners increases the chances of receiving the requested budget. While not necessarily complete, the following is a checklist of expense items that should be considered for an annual appraisal program:

Personnel Expenses

- Salaries

- Benefits

- Overtime

- In-house training

- Education

- Appraiser licensing and certification

Supply Expenses

- Office supplies

Professional Services Expenses

- Outside appraisal contract

- Mapping or GIS contract

- Data processing contract

- Temporary clerical

- Legal counsel

Communications Expenses

- Postage

- Telephone service

- Fax service

- Computer Network Fees

- On line data retrieval systems (Public access to data through the internet)

Travel and Transportation Expenses

- Property inspections

- Schools, workshops, seminars, conferences, meetings

- Vehicle maintenance and fuel

- Vehicle replacement

- Vehicle insurance

Advertising and Legal Notice Expenses

- Statutory notice of hearings concerning real and personal property protests

- Voluntary media releases, such as the senior citizen and veteran with a disability property tax exemptions or the personal property filing reminder

- Announcements of job vacancies

Computer and Office Equipment Expenses

- Purchase

- Rental or lease fees

- Repair and maintenance contracts

- Software and support

Other Specific Expenses

- Professional membership dues

- Printing

- Multiple Listing Service (MLS)

- Aerial Photographs

Selected References

Textbooks

Property Appraisal and Assessment Administration. International Association of Assessing Officers, Kansas City, 1990.

Property Assessment Valuation, Third Edition. International Association of Assessing Officers, Kansas City, 2010.

IAAO Technical Standards

Guide to Assessment Administration Standards, International Association of Assessing Officers, Kansas City, (August 2004).

Standard on Assessment Appeal, International Association of Assessing Officers, Kansas City, (July 2001).

Standard on Automated Valuation Models, International Association of Assessing Officers, Kansas City, (September 2003).

Standard on Contracting for Assessment Services, International Association of Assessing Officers, Kansas City, (December 2008).

Standard on Digital Cadastral Maps and Parcel Identifiers, International Association of Assessing Officers, Kansas City, (January 2009).

Standard on Facilities, Computers, Equipment, and Supplies, International Association of Assessing Officers, Kansas City, (September 2003).

Standard on Manual Cadastral Maps and Parcel Identifiers, International Association of Assessing Officers, Kansas City, ( August 2004).

Standard on Mass Appraisal of Real Property, (January 2011), International Association of Assessing Officers, Kansas City, (January 2011).

Standard on Oversight Agency Responsibilities, International Association of Assessing Officers, Kansas City, (July 2010).

Standard on Professional Development, International Association of Assessing Officers, Kansas City, (December 2000).

Standard on Property Tax Policy, International Association of Assessing Officers, Kansas City, (January 2010).

Standard on Public Relations, International Association of Assessing Officers, Kansas City, (January 2010).

Standard on Ratio Studies, International Association of Assessing Officers, Kansas City, (January 2010).

Standard on Valuation of Personal Property, International Association of Assessing Officers, Kansas City, (December 2005).

Standard on the Valuation of Properties Affected by Environmental Contamination, International Association of Assessing Officers, Kansas City, (July 2001).

Standard on Verification and Adjustment of Sales, International Association of Assessing Officers, Kansas City, (November 2010).

Other References

Tschohl, John. Achieving Excellence through Customer Service. Minneapolis: Best Sellers Publishing, 2002.

Garber, Peter R. 25 Reproducible Activities for Customer Service Excellence. Amherst: HRD Press, 2005.

Addendum 8-A, Workforce Analysis

In the late 1970s, homeowners concerned about skyrocketing residential property taxes pressured the state Legislature to address the problem. As a result, in 1982 Speaker of the House Bev Bledsoe appointed nine members from the General Assembly to study the problem and recommend solutions. The Legislature wanted to know what kind of impact biennial reappraisals would have on county assessors. The Division was asked to help with this analysis. A questionnaire concerning the additional workforce needs was mailed to each assessor, with a request to provide specific information to the Division. At the Law Seminar, Division employees interviewed assessors and captured the information needed to estimate the impact of biennial reappraisals. Those results were presented to the Legislature. The Workforce Study was born out of that process. Originally created in 1988, the workforce template has evolved over time. The latest revision was finalized in early 2018, analyzed and created with the help of a number of Category I through Category VI counties, and utilizes Excel.

The Division has two workforce analysis templates. The Comprehensive Workforce Analysis template is used when a study is conducted by Division staff. When a county conducts an independent study, the Limited Workforce Analysis template is used. It is highly recommended that prior to any presentation or implementation of the Limited Workforce Analysis the results be sent to the Division for review. An electronic copy of the template may be obtained from the Assessment Resources section of the Division.

The workforce template was created as a tool to assist the assessor in the analysis of staffing needs to perform the necessary duties of the assessor’s office. The template was not designed to account for any additional workforce needs for atypical yearly activities such as state board ordered reappraisal, database computer software changes, or a work backlog.

The template is only an analytical tool. The results are only as good as the information researched by the county. There is great diversity between the counties in Colorado with respect to characteristics such as county size, density of properties, computerization, task responsibilities, and numerous other factors. The default times for each task or activity in the template were developed with input from a variety of Category I through Category VI counties. Regardless of the county size, it is highly recommended that each assessor’s office research and develop its own time requirements for each activity listed. This will assure that the workforce analysis accurately represents the duties and responsibilities of the office and the personnel required to complete them.

General Template Instructions and Contents

The following instructions and (11) interrelated Excel worksheets are for use with the Limited Workforce Analysis template. The name of each worksheet below corresponds with the name of the template worksheet tabs.

| Worksheet Name and Description | Page | Worksheet “Tab” Name |

|---|---|---|

| Cover Sheet Identifies county name, date prepared, and Division and county staff. | na | COVER |

| Summary Displays total hours and staff needed for administrative and appraisal functions. Displays the appraisal review cycle. | Page 1 | SUMMARY |

| Administrative Data Gathering Worksheet Allows for entry of annual work units. Shows default time for each task. | Page 2 | ADMINISTRATIVE WORKSHEET |

| Administrative Time Requirement Estimate Worksheet Calculates the work hours for each task. A summary of required administrative staff is displayed. | Page 3 | ADMINISTRATIVE TIME |

| Administrative Calculations Converts the work hours to total administrative hours and total administrative FTE. | Page 4 | ADMINISTRATIVE CALCULATIONS |

| Abstract Data Gathering Worksheet Allows for entry of counts for each subclass. | Page 5 | ABSTRACT WORKSHEET |

| Cyclic Appraisal Worksheet Allows for entry of the appraisal review cycle for real property and the audit cycle for personal property. Combines certain subclasses that are included in the Cyclic Appraisal Review Cycle. | Page 6 | CYCLIC APPRAISAL WORKSHEET |

| Other Appraisal and Other Appraisal Functions Worksheet Combines certain subclasses that are included in Other Appraisal. Allows for entry of counts for Other Appraisal Functions. | Page 7 | OTHER APPRAISAL WORKSHEET |

| Appraisal Time Requirement Estimate Worksheet Shows subclasses included in the Cyclic Appraisal Review Cycle, Other Appraisal, and Other Appraisal Functions. Shows default times for each. | Page 8 | APPRAISAL TIME |

| Cyclic Appraisal Calculations Calculates the number of properties per subclass to receive an on-site cyclic review and an office review. Calculates total appraisal hours and total appraisal FTEs for each subclass receiving a cyclic review. | Page 9 | CYCLIC APPRAISAL CALCULATIONS |

| Other Appraisal and Other Appraisal Functions Calculation Converts the work hours to total appraisal hours and total appraisal FTE. A summary of required appraisal staff is displayed. | Page 10 | OTHER APPRAISAL CALCULATIONS |

Where to Begin: Basic Steps for Data Entry

Many cells and columns of the various template worksheets are locked and the template is password protected. This is necessary because many cells contain formulas that should not be inadvertently overridden for proper performance of the template. As you review the various worksheets, note that cells where data entry is necessary appear in red. Entries that are blue indicate the data was populated into the cell from another worksheet.

Step One: Create a back-up copy of the Excel template.

Step Two: On the Cover Worksheet, enter: the county name, the date of the study, and the county staff person(s) conducting the study. Once this information is entered, the date and county name populates to all of the worksheets in the template.

Step Three: On the Administrative Data Gathering Worksheet (page 2), enter the annual unit numbers for each of the listed administrative duties. The default times represent an average work time for each task. The Work Unit Time Measure column specifies if the default time is expressed in minutes or hours.

Entries for other administrative duties/tasks, other mapping tasks, and/or special projects are included to capture time spent on projects that are not identified in the template, such as scanning historical documents. The work time for these added tasks is entered on the Administrative Time Requirement Estimate Worksheet (page 3).

At the bottom of this worksheet is a box titled FTE Yearly Hour Calculation for Administrative and Appraisal Staff. Enter the hours worked in a typical day, the number of holidays, sick days, vacation days, days spent on in-house training for new programs/procedures (in-house training), and out-of-the office education days allowed for employees, on average. This information is used to calculate the number of full-time employees (FTEs) necessary to accomplish the required duties of the assessor’s office.

Step Four: The information from the Administrative Data Gathering Worksheet (page 2) and the Administrative Time Worksheet (page 3) populate the Administrative Calculations Worksheet (page 4). Note there is an office meeting head-count adjustment, which is calculated by formula, and captures the time for all staff to attend office meetings. (The calculation reflected under Office Management captures the time for one FTE.) The number of FTE hours and staff needed for to complete each administrative duty is automatically populated to the administrative section of the Summary (page 1).

The number of administrative FTEs, First-line supervision, and Top-level management is shown at the bottom of the Administrative Calculations Worksheet (page 4). When reviewing these staffing estimates, keep in mind, there are crossover duties where administrative staff complete appraisal duties and appraisal staff complete administrative duties.

Step Five: On the Abstract Data Gathering Worksheet (page 5), enter the parcel count data. Most of the needed counts come from the Abstract of Assessment. Other counts will require running reports and obtaining estimates from experienced employees. Cells highlighted in yellow; indicates the count cannot be obtained from the Abstract. Two cells are gray shaded; this indicates the field is prepopulated and an entry is not necessary. This information is transferred by formula to the other worksheets where appropriate.

Step Six: Most of the data on the Cyclic Appraisal Worksheet (page 6) is populated from the Abstract Data Gathering Worksheet (page 5). Data entry is required in the box labeled Appraisal Review Cycle. Refer to section Cyclic Appraisal for an explanation.

Step Seven: On the Other Appraisal and Other Appraisal Functions Worksheet (page 7), the parcel counts in the Other Appraisal section are populated from the Abstract Data Gathering Worksheet (page 5). The counts for the Other Appraisal Functions come from county staff knowledge and from reports generated by county staff. Entries for other appraisal duties/tasks, and/or special projects are included to capture time spent on projects that are not identified in the template. The work time for these added tasks is entered on the Appraisal Time Requirement Estimate Worksheet (page 8).

Step Eight: Work times for the cyclic appraisal tasks, other appraisal, and other appraisal functions are displayed on the Appraisal Time Requirement Estimate Worksheet (page 8). The work unit time measure identifies if the default time is minutes, hours, or some other measure. The cyclic appraisal section has two default times for each subclass. One for physical inspection and one for office review. The default times represent an average work time for each task. An explanation of cyclic appraisal is provided in the appraisal tasks section.

The work time for additional appraisal duties/tasks and special projects added on the Other Appraisal and Other Appraisal Functions Worksheet (page 7) is entered on this page.

Step Nine: The Cyclic Appraisal Calculations Worksheet (page 9) and the Other Appraisal and Other Appraisal Functions Calculations Worksheet (page 10) show the total appraisal hours and FTE needed for each task. Review these results. Note there is an office meeting head-count adjustment, which is calculated by formula, and captures the time for all staff to attend office meetings. (The calculation made for Office Meetings on page 8, captures the time for one FTE.)

The number of appraisal FTEs is shown at the bottom of the Other Appraisal and Other Appraisal Functions Calculations Worksheet (page 10) and entered into the appraisal section of the Summary (page 1). When reviewing the staffing estimates, keep in mind, there are crossover duties where administrative staff complete appraisal duties and appraisal staff complete administrative duties.

Step Ten: Review the Summary worksheet.

Printing the Template Pages

The individual worksheets that makeup the Comprehensive Workforce Analysis template are print-ready. In Excel, the following worksheets have been identified using Name Manager and can be accessed by using the Name Box.

- Cover

- Page1Summary

- Page2AdminGatheringWorksheet

- Page3AdminTimeEstimates

- Page4AdminCalculations

- Page5AbstractDataGatheringWorksheet

- Page6CyclicAprslWorksheet

- Page7OtherAppraisalandOtherFunctionWorksheet

- Page8AAprslTimeEstimate

- Page8BAppraisalTime

- Page9CyclicAprslCalc

- Page10OtherAprslandOtherAprslFunctionsCalc

The individual worksheets can be printed by selecting a page name from the Name Box (upper left below paste icon – drop down) and choosing print on the Print Menu. Note that when printing Pages 8A and 8B, select “print selection” on the Print Menu before choosing print. The whole template can be printed by choosing print on the Print Menu and selecting Entire Workbook. Page 8A must be separately printed.

Workforce Data

FTE Yearly Hour Calculation

Intrinsic to both the administrative and appraisal time estimates is the calculation of typical total full-time employee (FTE) yearly hours. The workforce template is designed to calculate the total yearly net hours.

The first step to calculating the net yearly hours is to determine the hours in a typical workday. The net daily hours is calculated by subtracting from the gross daily hours (typically 8 hours) any incidental non-work related time such as mandatory “work breaks.” The second is to determine the gross yearly days. This is calculated by multiplying the weeks in the year by the working days in a week, which typically results in 260 days (52 weeks per year times five days per week). Finally, the net yearly days is determined by subtracting holidays, typical employee sick and vacation days, new programs/procedures (in-house training), and out-of-office education and training days, from the gross yearly days. The new programs and procedures includes in-house training for new and existing appraisal staff, training for new programs enacted by legislation, additional computer training for new programs, and other similar duties.

The workforce template calculates the total net yearly hours. The net yearly hours per FTE is calculated by multiplying the net yearly days by the net daily hours. This figure represents the total net yearly hours that constitute full-time employment for a single employee. The required staff size can be estimated by dividing the total number of hours to complete all of the tasks necessary to operate the assessor’s office in a typical year by the total net yearly hours per FTE. This calculation is used for administrative and appraisal functions. The actual calculation is located at the bottom of the Administrative Data Gathering Worksheet (page 2).

Example:

The employees in Shine County work an eight-hour day (not including lunch), with two 15 minute mandatory work breaks, equaling a 7.5 hour workday. The county is closed for 10 holidays. The number of sick days is determined by averaging the number of sick days taken the previous year by all employees; it is determined that five days per employee are taken as sick leave. In-house training for new programs and procedures is estimated to be three days. There are 10 vacation days allowed for all full-time employees and the majority of the employees take the full 10 days each year. Based on the budgeted funding and the educational needs of staff, each employee is expected to spend 10 days each year in training. The computation of full-time employee (FTE) yearly hours is:

| Days | |

|---|---|

| Gross yearly work days | 260 |

| Holidays | -10 |

| Sick days (typical for the office) | -5 |

| Vacation days (typical for the office) | -10 |

| New programs/procedures (in-house training) | -3 |

| Education and training days | -10 |

| Yearly net days | 222 |

222 Days × 7.5 Hours (typical work day minus breaks, etc.) = 1,665 Yearly net hours

Work Units

The workload of an assessor’s office is separated between administrative and appraisal functions (tasks). For each of these tasks, a work unit type is defined. The work unit for each task is shown on each template worksheet. For appraisal functions, the parcel or schedule count is common. The administrative work unit may be the number of inquiries, subdivision plats, conveyance documents, tax increment financing areas, etc.

Work Time Estimates

An average time to complete each task in the template is listed as a default time. The default times for each task or activity were developed with input from a group of category I, II, III, IV, V, and VI counties. The Work Unit Time Measure column specifies if the default time is minutes or hours. The default times represent an average work time for each task.

Administrative Tasks

To establish appropriate work units and work time estimates for the administrative functions, the tasks are divided into these categories:

- Public Information

- Office Management

- Protest, Appeals, and Abatements

- Statutory Mailings

- Statutory Reports

- Data Control

- Forms Development and Approval

- Real Property Value Proration

- Movement of Titled Manufactured Homes

- State Assessed Properties

- Senior Citizen and Veteran with a Disability Exemptions

- Ownership Changes

- Sales Confirmation

- Address Changes

- Boundary Changes

- Tax Increment Financing

- Forest Land

- Create/Eliminate Property Subclass

- GIS/Mapping

- Computer System Maintenance

- Other Administrative Tasks/Duty and Special Projects

Administrative Functions

The following is a list of administrative functions (tasks) and work units for completing each task. Care should be taken when estimating the annual work units for each task. The yearly estimate would be greatly skewed if it were based on a week or month that was overly slow or busy.

Public Information

The public information section is divided into three categories: public inquiries, public inquiries requiring more extensive research/conversation, and public relations. Descriptions of each follow.

Public Inquiries

This category includes the normal, day-to-day requests for information received from the public in-person or by telephone. Such inquiries generally include use of parcel maps and ownership records, website information, or general taxation information. The work unit for these activities is the typical number of such requests per year and the work time estimate is an average of time spent. If records have not been kept for these activities, the annual work units can be estimated using the number of requests in the last week or month.

Public Inquiries Requiring More Extensive Research/Conversation

The category includes requests for information in-person, by telephone, or by letter that extend beyond the time allowed for a public inquiry. The work unit type for this activity is also the number of requests per year and can be estimated in the same manner as inquiries. The work time estimate is an average of time spent.

Some of the tasks that could be included in this activity are:

- Explaining the senior and veteran with a disability exemptions

- Providing information to the Division for legislative fiscal impact purposes

- Explaining personal property taxes to a new business owner

- Explaining the effect of proposed or newly enacted statutes or constitutional amendments to property owners or county officials.

Public Relations

This category includes time for specially planned public relations projects such as speeches, radio/television interviews, writing newspaper columns for the local newspaper, creating public notices and releases, and posting information on Facebook or a website. The work unit type is the number of occurrences per year and the work time estimate is an average amount of time spent.

Office Management

The office management section is broken into a number of categories. Descriptions of each follow.

Budget Preparation

Preparation of the assessor’s office budget is an annual event. The time for this activity should include: budget information gathering, prior year’s budget analysis, the analysis of future events or requirements that may cause additional budget needs, assessor budget meetings, and final budget report preparation and presentation. The work unit type is per year and the annual work unit is one. The work time estimate is the time spent by any staff involved in the process.

Budget Maintenance

Periodically reviewing the individual line items of the budget is a critical responsibility of the assessor or deputy assessor. Some counties may review their budget line items weekly while others review them monthly. The work unit type is per month and the work unit is 12. The work time estimate is the time spent by any staff involved in the review process. When the review occurs weekly, the work time estimate can be adjusted to accommodate the additional time.

Top Level Management

This category is used when the assessor or deputy assessor are not the primary supervisors of office staff. This category captures the time for the management of the assessor’s deputy assessor, chief administrative, and chief appraiser, contract employees, and other employees managed by the assessor or deputy assessor. The work unit is the number of employees managed. The work time estimate is the average time spent managing this group of employees per year, per employee. When this management/supervision structures does not exist, do not include a count entry for the task.

First-line Supervision of Administrative Staff

This category captures the time necessary for the supervision of the administrative personnel including performance monitoring, evaluation, hiring, and other related duties. The work unit is populated based on the calculation of FTE by the template. As workload data is added or modified, the FTE total automatically recalculates. The work time estimate is the average time spent on supervisory tasks per year, per employee.

Department Meetings

This includes such activities as attending regularly scheduled board of county commissioners meetings, general county budget hearings, meetings with the county clerk and the treasurer, county zoning meetings, or meetings with other department. The work unit type is the number of departments. The work time estimate for this activity is an average of the time spent.

Office Meetings

This includes in-house section and office meetings for the administrative staff. The annual work unit is the number of meetings per year and the work time estimate is an average of the time spent meeting with staff. The line-item calculation is the time for one staff person, consequently an office meeting head-count adjustment is made in the Administration Summary on the Administrative Calculations worksheet (page 4).

Office Support

This includes activities such as general correspondence, review and processing employee timesheets, payroll, processing travel expenses, tracking employee leave, county vehicle coordination, and other such support duties. The annual work unit is 52. The work time estimate is the time spent by any staff involved in the process, as several employees could share the duties.

Protests, Appeals, and Abatement Petitions

The protest and appeals section is broken into six categories and captures the administrative time spent handling protests, appeals, and abatement petitions. Descriptions of each follow.

- Protests to assessor: The administrative duties generally include a review of the protest, date-stamping the documents, determining if the protest was timely filed, entry into a protest log, and passing the protest to the appropriate appraisal staff. The annual work unit is an average number of the reappraisal year’s and the intervening year’s protests as reported on the Other Appraisal and Other Appraisal Functions Worksheet (page 7) and is populated by formula to the Administrative Data Gathering Worksheet (page 2). The work time estimate is the average time spent per protest.

- Appeals to County Board of Equalization (CBOE): This generally includes receiving hearing notice from the commissioner’s office, noting the hearing date in the file, and passing the file and appeal to the appropriate appraisal staff. The annual work unit is an average number of the reappraisal years and the intervening year’s CBOE appeals as reported on the Other Appraisal and Other Appraisal Functions Worksheet (7) and is automatically populated by formula to the Administrative Data Gathering Worksheet (page 2). The work time estimate is the average time spent per appeal.

- Appeals to Board of Assessment Appeals (BAA): This shows the administrative time spent handling appeals to the BAA, and includes tasks such as logging appeal and docket number, notifying the appropriate appraiser, assisting with the file preparation, and processing the final order. The annual work unit is reported on the Other Appraisal and Other Appraisal Functions Worksheet (page 7) and is populated by formula to the Administrative Data Gathering Worksheet (page 2). The work time estimate is the average time spent per appeal.

- Appeals to court: This accounts for the administrative time spent handling appeals and related duties for district court or appellant court hearings (Court of Appeals and Supreme Court). Tasks include logging appeal and court docket number, notifying the appropriate appraiser, and processing the final order. The annual work unit is reported on the Other Appraisal and Other Appraisal Functions Worksheet (page 7) and is populated by formula to the Administrative Data Gathering Worksheet (page 2). The work time estimate is the average time spent per appeal.

- Appeals to arbitration: The administrative duties can include tasks such as, logging the appeal, notifying the appropriate appraiser, assisting with the file preparation, and processing the final order. The annual work unit is reported on the Other Appraisal and Other Appraisal Functions Worksheet (page 7) and is populated by formula to the Administrative Data Gathering Worksheet (page 2). The work time estimate is the average time spent per appeal.

- Abatement petitions: This category includes tasks such as, review of the abatement petition, date-stamping the documents, determine if a protest was previously filed, determine if the filer has standing, forward the petition to the appropriate appraisal staff, track scheduled hearing, and enter decision. The annual work unit is an average number of abatement petitions filed in the reappraisal year and the intervening year, for all levels, as reported on the Other Appraisal and Other Appraisal Functions Worksheet (page 7) and is populated by formula to the Administrative Data Gathering Worksheet (page 2). The work time estimate is the average time spent per abatement petition.

Statutory Mailings

Computerization and outsourcing can have a significant impact on the work time necessary for each report. The work unit type is the number of mailings, the annual work unit is one for each mailing, and the work time estimate includes verification of information, proofreading, and preparation for mailing. The various mailings are listed below.

- Personal Property Declaration Schedules

- Subdivision Land Valuation Questionnaires

- Senior and Veteran Exemption Notices to owners

- Notices of Valuation for Real Property

- Notices of Valuation for Personal Property, Rigs, Producing Natural Resources

- Real Property Notices of Determination

- Personal Property, Rigs, Producing Natural Resources Notices of Determination

- Senior and Veteran Exemption Denials

Statutory Reports

Preparation of the statutory reports required by the assessor’s office is accounted for under this category. The work unit type is the number of reports, the annual work unit is one for each report, and the work time estimate includes generating reports, verification of information, proofreading, and preparation of the report. The various reports are listed below.

- Senior and veteran exemption data to Division (two downloads)

- Out-of-State Owners List

- CBOE report

- Abstract of Assessment

- Certification of Values

- Approved senior and veteran exemptions to Division (two downloads)

- Recertification of values

- Tax warrant

- Destroyed real property, personal property due to natural causes to county treasurer

Data Control Measures

Abstract (class and subclass) reports should be run at least on a monthly basis to assist the assessor in catching data input and program calculation errors. This may be a daily or monthly function in some counties. The following are examples of situations to verify. Internal codes that is not tied to a subclass code established by the Administrator, subclass code with a zero value, vacant land subclass code with improvement subclass code, exempt subclass code with taxable subclass code, and mismatched land and improvement classification codes.

Forms Development and Approval

The category includes the time required to review the forms requirements, create, edit, and submit forms for approval by the Division. Outsourcing can have a significant impact on the time. The annual work unit is the number of forms and the work time estimate is the average time per form.

Real Property Valuation Prorations

The category includes the administrative time required to prorate or apportion values for such transactions as destroyed property, changes in taxable status, and rotary drill rig value apportionment. The annual work unit is the number of prorations per year and the work time estimate is the average time per proration.

Movement of Titled Manufactured Homes

The category includes the administrative time required to complete or review an Authentication/Certification – Manufactured Home Tax form, identify tax area changes based on a location change or when the home is new to the county, create or change the property record, prorate the value if necessary, and pass the information to the appropriate appraiser if home is new to the county. The annual work unit is the number of homes that move per year and the work time estimate is the average time per movement.

State Assessed Properties

Typically, the records regarding state assessed companies are entered into the county database and maintained by administrative staff. This requires the entry of new companies, the distribution of values between real and personal property, value distribution to tax areas, verification and distribution of new construction values, confirmation of tax areas, and balancing entries to the notice of valuation. The time necessary to manage state assessed values can vary greatly depending on several factors such as the number of new companies vs. companies taxed the previous year, whether the breakdown between real and personal property is known or must be researched, the manner in which the state assessed values are apportioned to the correct tax areas or taxing entities, and the number of taxing entities or tax areas in the county. The annual work unit is the number of companies and the work time estimate is the average time per company. The category is broken down between existing companies and new companies.

Senior Citizen and Veteran with a Disability Exemptions

The category includes the administrative time required to review and approve or disapprove exemption applications, request additional information, review previously approved exemptions on other property, and remove the exemption status if necessary. The annual work unit is the number of exemption applications received and the work time estimate is the average time spent per application.

Ownership Changes

Ownership changes include processing all types of conveyance documents, including titled manufactured homes and severed mineral interests. The category is separated into two areas, straight transfer and split/combination.

Straight Transfer

Straight ownership transfers are the result of conveyance documents recorded in the clerk’s office that transfer property without any division of parcels or interests. It also includes verification of title application or copy of Certificate of Title/Ownership, which indicates the ownership transfer of a titled manufactured home. The annual work unit is the number of transfers per year. The average number can be estimated starting on a typical per-week or per-month basis and multiplying the count by the number of weeks or months per year to obtain the annual figure. The work time estimate is the average time spent per conveyance.

Split/Combination

Split/combination ownership transfers are the result of conveyance documents recorded in the clerk’s office that transfer a portion of a property or an interest in property. This includes identifying the conveyed portion of a parcel or the interest conveyed, writing legal descriptions, and creating new records. Severed mineral interests are included in this category. The annual work unit is the number of splits/combinations per year and the work time estimate is the average time spent per split/combination. The work time estimate does not include any appraisal or mapping duties.

Sales Confirmation

A sales confirmation program includes administrative activities such as mailing Real Property Transfer Declarations (TD-1000), Manufactured Home Transfer Declarations (MHTD), questionnaires, logging the returned documents, and sales coding them into the system. This entry does not include any appraisal time spent in sales confirmation or time that is accounted for in the property transfer process. The annual work unit is the number of sales confirmations handled yearly and is separated by type of declaration. The work time estimate is the average time spent per sale.

Address Changes

Processing all mailing address changes where there is no transfer of ownership is included in this function. The annual work unit is the number of address changes per year and the work time estimate is the average time spent per change.

NOTE: If the address changes are completed by another county office, do not include a count entry for the task.

Boundary Changes

Boundary changes result from documents recorded in the clerk’s office. The documents that cause boundary changes include subdivision plats, a court order creating a new taxing entity, annexation, inclusion, exclusion, and disconnection orders.

New Subdivision, Townhome, Condominium, and PUD Plats

This category accounts for the process of setting up new subdivisions and condominiums. It does not include mapping or appraisal duties. Mapping duties are included in GIS/Mapping and appraisal duties are captured in the appraisal functions. In the template, plats are separated into new subdivision plats (subdivisions, townhomes, and PUDs) and new condominium plats. The annual work unit is estimated based on the prior year’s activity and any reliable future projections. The work time estimate is the average time spent per plat.

New Taxing Entity

This category accounts for the process of setting up a new taxing entity and includes verification that the necessary documents were filed according to the statutory requirements, identifying real and personal property affected, and creating and modifying all records. Mapping duties are included in GIS/Mapping. The annual work unit is estimated based on the prior year’s activity and any reliable future projections. The work time estimate is the average time spent per new entity.

Annexation/Inclusion

This category accounts for the processing of annexation and inclusion orders and includes verification that the documents were filed according to the statutory requirements, determining the effective date, identifying real and personal property affected, and modifying all records. Mapping duties are included in GIS/Mapping. The annual work unit is estimated based on the prior year’s activity and any reliable future projections. The work time estimate is the average time spent per order.

Disconnection/Exclusion

This category accounts for the processing of disconnection and exclusion orders and includes verification that the documents were filed according to the statutory requirements, determining the effective date, identifying real and personal property affected, and modifying all records. Mapping duties are included in GIS/Mapping. The annual work unit is estimated based on the prior year’s activity and any reliable future projections. The work time estimate is the average time spent per order.

Tax Increment Financing